Gift funds are a very valuable and common strategy for first time homebuyers In today’s competitive housing market. Low inventory and high prices make it difficult for young adults to afford their first homes.

Fortunately, parents can play a crucial role in helping their children navigate these obstacles. In this blog post, we’ll explore two primary methods parents can use to assist their children: gift funds and the gift of equity.

Understanding Gift Funds

Gift funds are monetary gifts parents give to their children to help with the down payment and closing costs of a home. These funds can significantly reduce the financial burden on first-time buyers, making it easier for them to qualify for a mortgage. Here’s how gift funds work:

Eligibility: The gift must be from a family member.

Documentation: A gift letter must be provided, stating that the funds are a gift and do not need to be repaid.

Limitations: Some lenders have specific rules regarding how much can be gifted.

The Gift of Equity: A Lesser-Known Option

While gift funds are widely known, the gift of equity is another powerful tool that many parents and homebuyers are unaware of. This method involves parents selling their home to their children at a price below market value, effectively gifting the equity to their kids. Here’s a step-by-step breakdown of how it works:

Parents Purchase a New Home: Parents decide to move and purchase a new property.

Sell Current Home to Children: Instead of selling their existing home on the open market, parents sell it to their children.

Mortgage and Equity Gap: The children qualify for a mortgage, but it might not cover the full market value of the home. The difference, or equity gap, is gifted to the children.

Ownership Transfer: The children take ownership of the home with little to no money out of pocket.

Benefits of Gifting Equity

Reduced Financial Strain: Children can afford the home without needing a larger mortgage.

Family Wealth Transfer: Keeps the property and its value within the family.

Potential Tax Benefits: Utilizes the IRS’s lifetime giving limit to avoid taxation.

Addressing Tax Concerns

One common concern among parents considering a gift of equity is the potential tax implications. Here’s what you need to know:

Annual Gift Tax Exclusion: Parents can give up to $15,000 per year per child without triggering gift taxes.

Lifetime Giving Limit: As of 2024, the IRS allows a lifetime gift limit of over $13 million per person ($27 million for married couples). This limit includes the value of the gifted equity.

It’s essential to consult with a CPA to understand the specific tax implications and ensure compliance with IRS regulations.

Step-by-Step Guide to Gifting Equity

Evaluate the Home’s Market Value: Determine the current market value of the home.

Calculate the Mortgage Amount: Establish the mortgage amount your children can afford.

Determine the Equity Gap: Subtract the mortgage amount from the market value to find the equity gap.

Gift the Equity: Transfer the property to your children, gifting them the equity gap.

Handle Closing Costs: Consider rolling closing costs into the mortgage to minimize out-of-pocket expenses.

Final Thoughts

Helping your children buy their first home is a generous and impactful way to support their financial future. Whether through gift funds or a gift of equity, parents can make homeownership more accessible for the next generation. If you’re considering these options, it’s crucial to consult with mortgage professionals and tax advisors to navigate the process smoothly and maximize the benefits.

If you have any questions or need assistance with the details, please reach out to us at The Mortgage Architects. We specialize in helping families with these transactions and are here to guide you every step of the way.

FAQs: Helping Kids Buy Their First Home

Q1: What are gift funds?

A1: Gift funds are monetary gifts given by parents (or other family members) to their children to help with the down payment and closing costs of purchasing a home. These funds can reduce the financial burden on first-time buyers and make it easier for them to qualify for a mortgage.

Q2: Are there any restrictions on using gift funds for a down payment?

A2: Yes, gift funds must come from a family member and a gift letter must be provided to the lender. The letter should state that the funds are a gift and do not need to be repaid. Some lenders may have specific rules regarding the amount that can be gifted.

Q3: What is a gift of equity?

A3: A gift of equity occurs when parents sell their home to their children at a price below market value, gifting the difference in equity to their children. This allows the children to afford the home without needing a larger mortgage.

Q4: How does the gift of equity process work?

A4:

Parents purchase a new home.

They sell their current home to their children at a discounted price.

The children qualify for a mortgage, which may not cover the full market value.

The equity gap (difference between market value and mortgage) is gifted to the children.

The children take ownership of the home, often with little to no money out of pocket.

Q5: What are the benefits of gifting equity?

A5:

Reduces financial strain on children.

Keeps the property and its value within the family.

Utilizes the IRS’s lifetime giving limit to avoid gift taxes.

Q6: Are there any tax implications when gifting equity?

A6: Yes, but parents can give up to $15,000 per year per child without triggering gift taxes. Additionally, the IRS allows a lifetime gift limit of over $13 million per person ($27 million for married couples) as of 2024. This limit includes the value of the gifted equity. It’s advisable to consult with a CPA to understand specific tax implications.

Q7: What is the lifetime giving limit?

A7: The lifetime giving limit is the total amount a person can gift over their lifetime without incurring gift taxes. As of 2024, this limit is over $13 million per person, or $27 million for married couples.

Q8: Can closing costs be included in the mortgage when gifting equity?

A8: Yes, in many cases, closing costs can be rolled into the mortgage, reducing the need for out-of-pocket expenses from the children.

Q9: What should parents consider before deciding to gift equity?

A9: Parents should consider the financial readiness of their children, the impact on their own financial situation, and potential tax implications. Consulting with mortgage professionals and tax advisors is crucial to navigate this process smoothly.

Q10: How can parents start the process of gifting equity?

A10:

Evaluate the current market value of their home.

Determine the mortgage amount their children can afford.

Calculate the equity gap.

Decide on the amount of equity to gift.

Handle the property transfer and closing costs with the help of professionals.

Q11: Who should parents consult when considering gifting equity?

A11: Parents should consult with mortgage professionals, real estate agents, and tax advisors (CPAs) to ensure they understand all aspects of the process and to comply with legal and tax regulations.

Q12: How can The Mortgage Architects assist in this process?

A12: The Mortgage Architects specialize in helping families with transactions involving gift funds and gifts of equity. They can provide guidance, handle the paperwork, and ensure the process is smooth and compliant with all regulations. Contact them for personalized assistance.

If you have further questions or need detailed assistance, please reach out to us at The Mortgage Architects. We’re here to help you every step of the way.

Today, I want to address a common concern for many looking to buy a home: how to qualify for a mortgage using income from a future job. Let’s dive into the details to help you understand the process and avoid any pitfalls.

Why Future Employment Matters in Home Loans

When you’re planning to move for a new job and need a place to live, it can get tricky. Lenders are cautious when it comes to approving loans based on future employment. Here’s why:

Income Verification: Lenders need assurance that you will have a steady income to cover your mortgage payments.

Job Stability: They prefer salaried positions or guaranteed full-time hours to mitigate the risk of income variability.

Key Considerations for Using Future Employment Income

1. Salary vs. Variable Income

Salary Employment: It’s much easier to qualify if your new job offer includes a salary or guaranteed full-time hours. This stable income can be used to calculate your loan eligibility.

Variable Income: If your income includes overtime, bonuses, or commissions, it falls under variable income. In such cases, lenders require at least one pay stub showing this income before they can approve the loan.

2. Clearing Contingencies

Non-Contingent Offers: Your job offer should not be contingent on any conditions like background checks or drug tests. Lenders need confirmation that all contingencies are cleared.

Employer Letter: Obtain a letter from your employer stating that all contingencies have been met and you have a secure position.

3. Timing of Employment Start

Start Date Window: The start of your new job should be within 30 days before or after the loan closing date. This ensures lenders that you will have an income stream soon after closing.

Reserve Funds: You need to have enough reserve funds to cover your mortgage payments and other debts during any employment gap.

Steps to Ensure Loan Approval

Secure a Non-Contingent Job Offer: Make sure your offer letter states that your employment is not contingent on any pending conditions.

Provide Proof of Income: If you have variable income, ensure you can provide a pay stub that matches the income used to qualify for the loan.

Timing is Crucial: Align your job start date with the loan closing date within the 30-day window to meet lender requirements.

Maintain Reserve Funds: Keep sufficient funds in your account to cover mortgage payments and debts for the transition period.

Common Questions

What if I’m Moving to a Higher-Paying Job?

If your new job comes with a higher salary, it’s crucial to demonstrate that you can handle the increased mortgage payments. This involves showing adequate reserve funds and ensuring your income aligns with the lender’s calculations.

What Happens During an Employment Gap?

Lenders are wary of gaps in employment. Even if you plan to keep working until your new job starts, the lender needs assurance through your reserve funds. This helps them see that you can make payments even if there’s an unexpected job change.

Conclusion

Qualifying for a home loan with future employment income is possible, but it requires careful planning and documentation. Ensure your job offer is non-contingent, align your employment start date with the loan closing date, and maintain sufficient reserve funds. By following these steps, you can navigate the process smoothly and secure your dream home.

If you have any more questions or need further assistance, feel free to reach out. Have a great day!

When is the right time to do a refinance? This is a question I get a lot at Mortgage Architects, especially as interest rates begin to come back down after a couple of years of increases.

Timing the Market

One of the first things to understand about refinancing is that it’s nearly impossible to perfectly time the market. You might get lucky and hit the exact bottom of the interest rate cycle, but it’s more likely that you won’t. Instead, the goal should be to refinance when rates come down to a favorable level. This approach helps mitigate the risk of rates spiking unexpectedly due to factors like inflation.

Why Timing is Tricky

Market Volatility: Economic conditions can change rapidly, affecting interest rates.

Inflation: Persistent inflation can keep rates high for extended periods.

Global Events: Unpredictable global events can also influence interest rates.

Refinancing Strategy

When considering a refinance, it’s important to have a strategic approach. Let’s explore the best practices and what to avoid.

Avoid Overly Aggressive Rate Cuts

Imagine you have a current mortgage on a $650,000 property with a loan amount of $413,000 at an interest rate of 7.625%. If you refinance aggressively to drop the interest rate by a full percentage point, the new loan amount might increase to $422,000. This increase can be problematic for several reasons:

Increased Loan Amount: Adding to your loan amount means higher monthly payments and more interest paid over time.

Future Rate Drops: If rates continue to fall, refinancing again will add even more to your loan amount, compounding the problem.

A Balanced Approach

A more balanced approach would be to reduce the interest rate by five-eighths of a point instead. This method offers significant savings without excessively increasing your loan amount. For example, this could save you $180 per month while only adding about $3,000 to your loan.

Managing Added Loan Amount

If you do end up adding to your loan amount, there are strategies to mitigate this impact.

Skipping a Payment

When you refinance, you typically skip one monthly payment. Instead of pocketing this amount, apply it to your new loan. For instance, if your skipped payment is $3,421, applying it to your new loan immediately reduces the added amount.

Escrow Adjustments

Your new lender will collect escrows for taxes and insurance, which initially increases your loan amount. However, your old lender will refund the previously collected escrows. Apply this refund to your new loan, further reducing the balance.

Continuous Refinancing Strategy

One effective strategy is to refinance every six to seven months, following the interest rates down. After making six monthly payments on your new loan, you can refinance again. This method allows you to progressively lower your interest rate and loan amount over time.

Cash-Out Refinancing

Another consideration is cash-out refinancing, especially if you have high-interest debt. For example, if you have credit card debt with rates in the 20-30% range, a cash-out refi can be a smart move. Even if your mortgage rate is relatively low, using the equity in your home to pay off high-interest debt can save you a significant amount of money and improve your financial stability.

Benefits of Cash-Out Refinancing

Debt Consolidation: Pay off high-interest debt.

Credit Improvement: Reduce your credit utilization ratio, potentially boosting your credit score.

Financial Flexibility: Gain more control over your monthly cash flow.

Conclusion

Refinancing can be a powerful financial tool when done strategically. Whether you’re aiming to lower your interest rate or consolidate debt, it’s important to approach refinancing with a clear plan and avoid overly aggressive tactics that could increase your loan amount unnecessarily. If you have any questions or would like to see what refinancing could look like for your specific situation, feel free to reach out to us at Mortgage Architects. We’re here to help you navigate the complexities and make the best decision for your financial future.

Key Takeaways

Timing: Refinance when rates are favorable, but don’t aim for perfection.

Strategy: Avoid aggressive rate cuts that significantly increase your loan amount.

Manage Loan Amount: Use skipped payments and escrow refunds to reduce added amounts.

Continuous Refinancing: Follow interest rates down by refinancing every six to seven months.

Cash-Out Refi: Consider for high-interest debt to improve financial health.

We’ll be happy to build out a personalized refinancing scenario for you. Talk to you soon!

FAQs on Refinancing Your Mortgage

What is refinancing?

Refinancing involves replacing your current mortgage with a new one, usually to take advantage of lower interest rates, change the loan term, or access home equity.

When is the best time to refinance?

The best time to refinance is when interest rates are lower than your current mortgage rate. However, timing the market perfectly is challenging, so it’s advisable to refinance when rates are favorable rather than trying to hit the exact bottom.

What are the benefits of refinancing?

Refinancing can lower your monthly mortgage payments, reduce your interest rate, shorten your loan term, or allow you to access the equity in your home for other financial needs.

What should I avoid when refinancing?

Avoid overly aggressive rate cuts that significantly increase your loan amount. This can lead to higher monthly payments and more interest paid over time, especially if you plan to refinance again in the future.

How often can I refinance my mortgage?

You can refinance your mortgage as often as it makes financial sense. Generally, it’s advisable to refinance every six to seven months if rates are consistently falling, allowing you to follow the rates down and continually improve your loan terms.

What is a cash-out refinance?

A cash-out refinance allows you to take out a new mortgage for more than you owe on your current one, receiving the difference in cash. This can be useful for consolidating high-interest debt, such as credit card balances, at a lower mortgage rate.

Will refinancing affect my credit score?

Refinancing can temporarily lower your credit score due to the credit inquiry and the new account on your credit report. However, if refinancing reduces your debt or improves your financial situation, it can positively impact your credit score in the long run.

What are the costs associated with refinancing?

Refinancing costs can include application fees, appraisal fees, title insurance, and closing costs. It’s important to compare these costs with the potential savings from a lower interest rate to determine if refinancing makes financial sense.

How do skipped payments and escrow adjustments affect refinancing?

When you refinance, you usually skip one monthly payment, which can be applied to your new loan to reduce the principal. Additionally, your new lender will collect escrows for taxes and insurance, but your old lender will refund the previously collected escrows. Applying this refund to your new loan can further reduce the balance.

Can I refinance if I have bad credit?

Refinancing with bad credit can be challenging, but it’s not impossible. You may need to explore options like FHA loans or find a co-signer. Additionally, improving your credit score before refinancing can help you secure better terms.

What if I have a high amount of credit card debt?

If you have high-interest credit card debt, a cash-out refinance can be a smart move. Using the equity in your home to pay off high-interest debt can save you money and improve your financial stability. After the cash-out refinance, you can follow the strategy of refinancing to lower your mortgage rate as interest rates fall.

How do I start the refinancing process?

To start the refinancing process, contact your mortgage lender or a mortgage broker to discuss your options. They can help you compare different loan products and determine the best refinancing strategy for your financial situation.

How can I determine if refinancing is right for me?

Refinancing is a personal decision that depends on your financial goals, current mortgage terms, and market conditions. Consulting with a mortgage professional can help you evaluate your situation and decide if refinancing is the right move for you.

House hacking with an FHA loan lets you buy a multi-unit property, live in one unit, and rent out the others—so your tenants help cover your mortgage. This guide breaks down the FHA house hacking rules and limits, how the self-sufficiency test works for 3–4 unit properties, and how rental income can help you qualify. You’ll also see practical scenarios to illustrate how this strategy can reduce monthly housing costs and help you start building a real estate portfolio.

Understanding House Hacking

House hacking involves purchasing a property with multiple units and living in one while renting out the others. This approach allows homeowners to use rental income to offset mortgage payments and other housing costs. For first-time homebuyers, using an FHA loan can make this process even more accessible due to its lower down payment requirements.

FHA House Hacking Rules & Limits (Quick Guide)

Here are the most common rules and limits buyers should understand before pursuing an FHA house hack:

Owner-occupancy is required. You must live in the property as your primary residence (you can’t buy a multi-unit purely as an investment property with FHA).

House hacking is typically done with 2–4 unit properties. Duplexes, triplexes, and fourplexes are common for FHA house hacking.

3–4 unit properties require the FHA self-sufficiency test. FHA uses a rental income test to confirm the property can support itself financially (details below).

Rental income is typically counted with a vacancy factor. FHA and lenders commonly use a reduced portion of rent (often 75%) to account for vacancies and upkeep.

Loan limits apply. FHA borrowing limits vary by county and property type (2–4 units often have different limits than single-family homes).

Property standards matter. FHA appraisals can be stricter about condition and safety, which can influence which properties qualify.

If you want, we can run a quick scenario based on your target price range and estimated rents to see what’s realistic.

Key Benefits of House Hacking

Lower Monthly Expenses: Rental income from additional units can cover a significant portion of the mortgage payment.

Building a Real Estate Portfolio: House hacking is an excellent way to start investing in real estate without needing substantial upfront capital.

Increased Purchase Power: Rental income can help buyers qualify for larger loans.

FHA Loans vs. Conventional Loans

FHA loans require a down payment of just 3.5%, making them an attractive option for first-time buyers. Recently, Fannie Mae and Freddie Mac updated their guidelines to allow conventional loans to be used for multi-unit properties with a down payment as low as 5%. However, each loan type has its nuances.

FHA Loan Highlights

Lower Down Payment: 3.5% down payment requirement.

Interest Rates: Typically lower than conventional loans.

Self-Sufficiency Test: Required for properties with three or more units, ensuring that the property generates enough rental income to cover mortgage payments.

Conventional Loan Highlights

Down Payment: 5% down payment requirement.

Interest Rates: Typically higher than FHA loans.

No Self-Sufficiency Test: Makes it easier to qualify for larger multi-unit properties.

Reserve Requirements: Requires six months of reserves, which can include retirement accounts.

Practical Scenarios

To better understand the benefits and challenges of house hacking, let’s explore a few scenarios.

Scenario 1: Single-Family Residence

Current Rent: $1,500/month

Purchase Price: $280,000

Down Payment (3.5%): $9,800

Interest Rate: 6.25%

Monthly Mortgage Payment: $2,400

Scenario 2: Two-Unit Building

Purchase Price: $350,000

Down Payment (3.5%): $12,250

Interest Rate: 6.25%

Monthly Mortgage Payment: $3,000

Rental Income from Second Unit: $1,500

Net Monthly Expense: $1,500

Scenario 3: Three-Unit Building

Purchase Price: $400,000

Down Payment (3.5%): $14,000

Interest Rate: 6.25%

Monthly Mortgage Payment: $3,400

Rental Income from Two Units: $3,000

Net Monthly Expense: $400

The Self-Sufficiency Test

For a three- or four-unit property, the FHA loan requires a self-sufficiency test. This test mandates that 75% of the rental income from the property must exceed the monthly mortgage payment, including HOA dues.

Total Rental Income: $4,500 (assuming $1,500 per unit)

75% of Rental Income: $3,375

Monthly Mortgage Payment: $3,370

In this scenario, the property just passes the self-sufficiency test.

Conventional Loan Considerations

Switching to a conventional loan for a $400,000 property means no self-sufficiency test, but higher interest rates and mortgage payments. The buyer would also need six months of reserves, which could come from cash savings or retirement accounts.

Conclusion

House hacking with FHA loans offers a powerful strategy for first-time homebuyers to enter the real estate market, reduce monthly expenses, and start building wealth through property ownership.

By understanding the differences between FHA and conventional loans and considering the specific requirements and benefits of each, buyers can make informed decisions that align with their financial goals.

If you have any questions or need personalized advice, feel free to reach out to us. We’re here to help you navigate the complexities of real estate investment and find the best solution for your needs.

Frequently Asked Questions (FAQ) about House Hacking with FHA Loans

What is house hacking?

House hacking is a strategy where you purchase a property with multiple units and live in one while renting out the others. The rental income from the additional units helps offset your mortgage payments and other housing costs.

Why use an FHA loan for house hacking?

FHA loans are popular for house hacking because they require a lower down payment (3.5%) compared to conventional loans. This makes it easier for first-time homebuyers to afford a multi-unit property.

What is the minimum down payment for an FHA loan?

The minimum down payment for an FHA loan is 3.5% of the purchase price.

What are the recent changes to conventional loan guidelines?

As of November 18th, 2023, Fannie Mae and Freddie Mac have updated guidelines allowing conventional loans to be used for multi-unit properties with a down payment as low as 5%.

What is the self-sufficiency test for FHA loans?

The self-sufficiency test is required for FHA loans on properties with three or more units. It ensures that 75% of the rental income from the property is enough to cover the monthly mortgage payment, including HOA dues.

How is rental income calculated for the self-sufficiency test?

Rental income is calculated based on an appraisal of the property. For the self-sufficiency test, only 75% of the total rental income is considered to account for potential vacancies and maintenance costs.

What are the pros and cons of using a conventional loan for house hacking?

Pros: No self-sufficiency test. Potentially easier qualification for larger properties. Cons: Higher interest rates compared to FHA loans. Higher mortgage insurance costs based on credit score. Requires six months of reserves, which can include cash savings or retirement accounts.

How does house hacking help build a real estate portfolio?

By purchasing a multi-unit property and using rental income to cover mortgage payments, homeowners can save money and potentially reinvest in additional properties. This strategy allows for the gradual building of a real estate portfolio with minimal upfront capital.

What should I consider before deciding between an FHA and a conventional loan?

Consider the following factors: Down Payment: FHA loans require 3.5%, conventional loans require 5%. Interest Rates: FHA loans generally have lower interest rates. Self-Sufficiency Test: Required for FHA loans on properties with three or more units. Reserve Requirements: Conventional loans require six months of reserves. Overall Costs: Factor in mortgage insurance and monthly payments.

Can rental income help me qualify for a larger loan?

In many cases, yes—rental income from the additional unit(s) can help strengthen your application and increase your purchasing power. Here are the most important considerations:

Rent figures are usually supported by the appraisal. Lenders often rely on the appraisal’s market rent estimate (and sometimes existing leases) to document rental income. A vacancy factor is typically applied. It’s common for lenders/programs to use a reduced portion of rent (often 75%) to account for vacancies and maintenance. For 3–4 unit properties, the self-sufficiency test can be a deciding factor. FHA requires the property to demonstrate it can support the monthly payment using a portion of the projected rental income.

If you’d like, share your target price range and property type (2-unit, 3-unit, or 4-unit) and we can run a quick scenario to estimate payment offset and qualifying strength.

If you’re reading this, chances are you’re a buyer who’s out in the market and trying to figure out whether or not you need a buyer’s agent. This decision has become even more crucial after the recent post-NAR (National Association of Realtors) ruling, which may mean that the home you’re purchasing will no longer cover the buyer’s agent commission, leaving you responsible for it.

This has caused a lot of fear and anxiety, making people wonder whether a buyer’s agent is really worth it. Let’s delve into why having a buyer’s agent can be a game-changer in your home-buying journey.

The Value of a Buyer’s Agent

An Advocate for Your Best Interests

Having someone paid to look out for your best interests is invaluable. Think about it: you wouldn’t represent yourself in court, right? Of course not. So, if you’re making a purchase worth hundreds of thousands of dollars, involving signed contracts that could potentially lead to legal issues, it makes sense to have a professional looking out for you. A buyer’s agent does just that.

Expert Negotiation Skills

A skilled buyer agent is worth their weight in gold, especially when it comes to negotiation. Whether it’s helping you land your dream home at the perfect price or negotiating the best purchase price on a hidden gem, their expertise is crucial. They can also negotiate favorable terms and seller concessions, which can save you a significant amount of money.

Buyer Agent Unbiased Perspective

It’s easy to fall in love with a house and overlook potential issues. A buyer’s agent provides an unbiased perspective, pointing out flaws that you might miss due to emotional attachment. For instance, they can spot mold or structural issues that could turn into nightmares after you move in.

Knowledge of the Market

A good buyer’s agent knows the local market inside and out. They understand home values, market conditions, and what it takes to get under contract in your desired area. This knowledge can prevent costly mistakes, such as purchasing a home in the wrong school district or overpaying for a property.

Identifying Red Flags

Buyer’s agents are trained to spot potential issues before they become costly problems. They can identify sloping floors, foundation cracks, and other structural issues that you might miss. This can save you from spending money on inspections for homes that aren’t worth pursuing.

Education and Guidance

Most people aren’t experts in the real estate buying process. A buyer’s agent provides education and guidance, helping you understand each step and reducing your anxiety. Their expertise ensures a smooth, seamless process from start to finish.

Addressing Common Misconceptions

Commission and Costs

A quick misnomer: you cannot use seller concessions to pay for the buyer agent commission, at least not yet. However, don’t fear—we have a commission gap strategy to help you navigate this challenge. Check out the details on our website for more information.

Emotional Detachment

It’s important to have someone involved in the deal who isn’t emotionally tied to it. A buyer’s agent can provide objective advice and ensure you make decisions based on logic and facts rather than emotions.

Local Expertise

Family members or friends from other parts of the country might offer advice, but real estate markets vary greatly by location. A buyer’s agent who lives and works in your desired area will have the local expertise needed to navigate that specific market.

Conclusion

In conclusion, a buyer’s agent offers numerous benefits that can save you time, money, and stress. From expert negotiation skills and market knowledge to identifying red flags and providing education, their value cannot be overstated. At The Mortgage Architects, we partner with top buyer’s agents to ensure a seamless, anxiety-free home-buying process. Reach out to us with any questions, and we look forward to seeing you at the closing table.

FAQ: Buyer Agent or No Buyer Agent

1. What is a buyer’s agent?

A buyer’s agent is a real estate professional who represents the interests of the buyer in a property transaction. They help buyers find suitable homes, negotiate terms and prices, and navigate the entire buying process.

2. Why do I need a buyer’s agent?

A buyer’s agent offers numerous benefits, including expert negotiation skills, market knowledge, the ability to spot potential issues, and providing objective advice. They help ensure you make informed decisions and avoid costly mistakes.

3. How is a buyer’s agent different from a seller’s agent?

A seller’s agent, or listing agent, represents the interests of the seller in a real estate transaction. A buyer’s agent, on the other hand, represents the buyer, ensuring their needs and interests are prioritized.

4. Will I have to pay the buyer’s agent commission?

After the post-NAR ruling, the home you’re purchasing may no longer cover the buyer’s agent commission, meaning you could be responsible for it. However, there are strategies to manage this cost effectively.

5. Can seller concessions be used to pay for the buyer agent commission?

Currently, seller concessions cannot be used to pay for the buyer agent commission. However, we have developed a commission gap strategy to help you navigate this issue.

6. How does a buyer’s agent help with negotiations?

A skilled buyer’s agent can negotiate the best price for your desired home, help you win against competition, and secure favorable terms and seller concessions. Their expertise can save you significant money and stress.

7. What kind of market knowledge does a buyer’s agent provide?

A buyer’s agent understands local market conditions, home values, and competition. They can guide you to the best neighborhoods, ensure you don’t overpay, and help you avoid areas with potential issues.

8. How can a buyer’s agent identify potential issues in a home?

A buyer’s agent is trained to spot red flags, such as structural issues, mold, or other problems that you might overlook. This can save you from making a costly mistake and investing in a problematic property.

9. What if I have family members or friends offering advice on my home purchase?

While well-meaning, advice from family or friends who are not familiar with your local market can be misleading. A buyer’s agent with local expertise can provide accurate, relevant guidance tailored to your specific area.

10. How does a buyer’s agent help reduce my anxiety during the buying process?

A buyer’s agent provides education, guidance, and support throughout the entire buying process. They help you understand each step, keep you grounded, and ensure a smooth, seamless experience, reducing your anxiety.

11. What should I look for in a good buyer’s agent?

Look for a buyer’s agent with strong negotiation skills, local market knowledge, a track record of successful transactions, and excellent communication. They should be committed to representing your best interests and providing objective advice.

12. How can I get in touch with a buyer’s agent?

Reach out to The Mortgage Architects for recommendations on trusted buyer’s agents in your area. We partner with top agents to ensure a seamless home-buying process for our clients.

13. What is the next step if I decide to use a buyer’s agent?

Contact us at The Mortgage Architects to discuss your needs and get connected with a qualified buyer’s agent. They will guide you through the next steps and help you start your home-buying journey.

Finding the best mortgage brokerage can seem like an overwhelming task, but fear not! 🌟 2026 is shaping up to be a great time to secure a mortgageor a refinance, and we’re here to guide you through the process. With a plethora of mortgage lenders and loan options available, it’s crucial to compare lenders and loan options to make the most informed decision for your homebuying journey. So buckle up and get ready to find the best mortgage brokerage of 2026! 🏡✨

In this article, you’ll discover the top mortgage bank lenders, understand mortgage brokers vs. banks, learn about the importance of credit scores and down payments, navigate the mortgage process with a brokerage, and much more. By the end, you’ll be well-equipped to choose the right mortgage brokerage and secure the best loan terms for your dream home. 🚀

Short Summary

Find the best mortgage brokerage of 2026 by evaluating reputation, loan options, and customer service.

Get personalized advice from a mortgage broker to find the ideal loan for your financial situation.

Improve your credit score & save for a down payment to get better terms on your mortgage.

Top Mortgage Brokerages of 2026

As you embark on your quest to find the best mortgage brokerage, it’s essential to consider the top players in the market and understand the differences between a bank lender and an independent mortgage broker.

Some of the most popular banking mortgage lenders of 2026 include:

Rocket Mortgage

Ally Bank

Fairway Independent Mortgage Corporation

LoanDepot

Better.com

Mr. Cooper

New American Funding

Flagstar Bank

PNC Bank

Chase

PenFed

These best mortgage lenders have been judged based on factors such as customer service, loan options, and competitive rates offered by each mortgage lender.

For instance, Chase stands out by offering competitive interest rates, loan programs for those with smaller down payments, and quick closings. On the other hand, Better.com is known for its completely digital process, great rates, and a vast array of loan options.

As you explore these top mortgage lenders, keep in mind the various factors that contribute to their success, and choose a lender that best aligns with your needs and preferences.

Looking ahead, the mortgage lenders of 2026 are anticipated to continue this trend of excellence, offering competitive loan options, exceptional customer support, and favorable terms that cater to a wide range of borrower needs. This forward-looking perspective suggests that whether you’re finalizing your choice now or later in the year, the quality and service of top mortgage lenders will remain a constant.

Mortgage broker vs. banks

When seeking a mortgage, it’s important to understand the differences between mortgage brokers and banks. A mortgage broker acts as a middleman between borrowers and lenders, helping borrowers determine which lender is best for them. On the other hand, a bank is a financial institution that lends money directly to borrowers. Mortgage brokers have access to loan programs and interest rates from multiple lenders, offering borrowers a more extensive range of options. 🤝

While both mortgage brokers and banks can provide home loans, there are some advantages to working with a mortgage broker. Mortgage brokers have more experience in the industry and can offer personalized advice and guidance to borrowers. Additionally, they have access to different loan programs and interest rates from various lenders, giving borrowers a wider range of choices to find the best fit for their needs.

Factors to consider when choosing a bank or brokerage:

Reputation: Review their background, customer feedback, and any awards or recognition they’ve received to assess their performance and credibility in the market.

Loan options: Consider the variety of loan options they offer and whether they can meet your specific needs.

Customer service: Look for a brokerage that provides excellent customer service and is responsive to your inquiries and concerns.

By considering these factors, you can make an informed decision when choosing a mortgage brokerage. Learn more about mortgage brokerages vs banks in this article: Should I Use a Mortgage Broker: Pros and Cons.

Moreover, it’s essential to explore a brokerage’s loan options, such as fixed-rate, adjustable-rate, and jumbo loans. A diverse range of loan options allows you to select the best-suited mortgage for your financial situation. 💼

Additionally, prioritize brokerages that provide personalized service, prompt responses, and consistent communication. By considering these factors, you’ll be well on your way to finding the perfect mortgage brokerage for your needs. 🏡✨

5 Tips to Find the Best Mortgage Brokerage

To further aid your search for the ideal mortgage brokerage, consider these five tips:

Ask your real estate agent for referrals. They are familiar with the local market and can recommend reputable brokers. 🏠

Research potential mortgage brokers online using platforms like Facebook, Google Business, Yelp, Better Business Bureau, and Trust Pilot. 🔍

Contact mortgage brokers and inquire about their experience, qualifications, fees, and services. Also, ask about their process for getting a loan approved. 📞

Ensure the mortgage broker you choose is licensed and insured, indicating they are qualified and experienced in handling your loan. 📜

Check if the mortgage broker is accredited by any industry bodies and has experience in the field, ensuring they are knowledgeable and up-to-date with the latest regulations and trends. 🏅

Understanding Mortgage Brokers

Mortgage brokers play a crucial role in the homebuying process, acting as intermediaries between borrowers and lenders, and helping you find the best rate and terms for your mortgage. One of the main perks of working with a mortgage broker is that they:

Search for the most competitive rates and terms on your behalf, saving you time and effort. 🕒

Provide personalized advice and guidance throughout the mortgage application process. 🗣️

Have access to a wide network of lenders, increasing your chances of finding the right mortgage for your needs. 🌐

Help you navigate complex paperwork and ensure all necessary documents are submitted correctly. 📄

Can assist with negotiating better terms and conditions with lenders. 💬

Allow you to focus on other important aspects of the homebuying process, such as searching for the perfect property and preparing for the big move. 🏡

By working with a mortgage broker, you can streamline the homebuying process and increase your chances of securing a favorable mortgage.

To get started on the mortgage process, gather all the necessary paperwork, such as income statements, bank statements, and other financial documents. This will help streamline the process and enable your mortgage broker to find the best options swiftly. 📑✨

When working with a mortgage broker, it’s essential to understand how they are compensated. Mortgage brokers are paid through a fee for their service, which is usually a small percentage of the loan amount. This fee can either be covered by the borrower or the lender. 💸

It’s important to note that the fee can increase the total cost of the loan, so it’s worth reviewing the fee structure before committing to a specific mortgage broker. By understanding how mortgage brokers are paid, you can make a more informed decision when choosing a brokerage to work with. 🧐📊

Mortgage Loan Programs Offered by Brokerages

Mortgage brokerages offer a variety of loan programs to suit the diverse needs of borrowers. Some common mortgage loans available through brokerages include:

Conventional loans

Jumbo loans

FHA loans

VA loans

USDA loans

Reverse loans

More niche loan programs (e.g., ITIN, Fix & Flip, Alternative Income, and more)

By working with a mortgage brokerage, you can explore various loan options to find the ideal mortgage for your financial situation.

For example, conventional mortgages are the most common type of home loan and are not backed by any government agency, such as the Federal Housing Finance Agency. On the other hand, government-backed loans, such as FHA, VA, and USDA loans, are backed by the federal government and may have more relaxed credit score requirements and lower down payment options. By understanding the different loan programs offered by mortgage brokerages, you can make a more informed decision when selecting a mortgage.

This approach helps you navigate the complex mortgage landscape with more confidence!

Specialty loans available at mortgage brokerages

In addition to conventional and government-backed loans, some mortgage brokerages offer unique loan options to cater to specific borrower needs. For instance, renovation loans 🔨🏠 are designed for borrowers looking to purchase a property that requires significant repairs or improvements. These loans allow you to borrow additional funds for the necessary renovations, simplifying the financing process.

Other niche programs may be available at certain mortgage brokerages, such as loans tailored for medical professionals with student loan debt or first-time homebuyers with limited down payment funds. By exploring these specialty loans, you can find a mortgage that is tailored to your unique needs and financial situation.

Evaluating Mortgage Interest Rates and Fees

Understanding and comparing mortgage interest rates and fees is crucial in determining the overall cost of a loan. The mortgage interest rate is expressed as a percentage of the overall loan amount. This represents the yearly cost of borrowing money. These rates can fluctuate, so it’s essential to regularly monitor the market and compare rates from different lenders to secure the best possible mortgage terms. 📊🔍

Aside from interest rates, it’s also vital to consider the various fees associated with a mortgage, such as lender fees, origination fees, and closing costs. These fees can significantly impact the total cost of your mortgage, so it’s important to review and compare them when selecting a mortgage brokerage or lender. 💰📝

Tips for negotiating lower rates and fees

To secure the best possible mortgage rates and minimize fees during the loan process, consider the following strategies:

Obtain loan estimates from a broker who will shop the market for you, so you don’t have to. This will enable you to compare interest rates and fees, ensuring you find the best deal for your needs.

Improve your credit score by staying on top of bills, reducing debt, and avoiding new credit checks. A higher credit score can help you qualify for better mortgage rates.

Be upfront and provide all the necessary documentation, such as income statements and bank statements, to streamline the mortgage process.

Understand the fees that the seller might be responsible for, such as closing costs and transfer taxes, and negotiate these costs when possible.

By employing these tactics, you can negotiate lower rates and fees, making your mortgage more affordable and suited to your financial needs. 💰✨

Importance of Credit Score and Down Payment

Your credit score and down payment play a significant role in the mortgage process. Here are some key points to consider:

A good credit score can secure you a better interest rate.

A larger down payment can help you avoid private mortgage insurance (PMI).

Both factors can greatly impact your loan eligibility and the terms of your mortgage.

To find the best mortgage for your needs, it’s essential to understand the minimum credit score requirements for different loan types and the down payment options available. By focusing on improving your credit score and saving for a down payment, you are more likely to secure a mortgage with favorable terms and rates.

Improving your credit score

Boosting your credit score is one of the most effective ways to secure better mortgage terms and rates. Here are some tips for improving your credit score:

Pay your bills on time by setting up auto payments or reminders.

Keep your credit utilization rate low by using only a small portion of your available credit.

Maintain old accounts to show a longer credit history and responsible credit management.

Regularly review your credit reports for mistakes and dispute any errors you find.

By following these tips, you can improve your credit score and increase your chances of securing a mortgage with favorable terms.

Saving for a down payment

Accumulating the necessary funds for a mortgage down payment is a crucial step in the homebuying process. Here are some strategies to help you save for a down payment:

Set up an automatic savings plan to consistently put money aside for your down payment.

Cut back on expenses and prioritize saving for your down payment over non-essential purchases.

Take advantage of employer-sponsored savings plans, such as 401(k) plans or other retirement accounts, to save for your down payment.

By implementing these strategies, you can save for a down payment more effectively and be better prepared to enter the mortgage process. 💼🏠

Navigating the Mortgage Process with a Brokerage

Working with a mortgage brokerage can simplify the homebuying process and help you find the best mortgage terms for your needs. By collaborating with your chosen brokerage and following their guidance, you can navigate the mortgage process more efficiently and with greater confidence. 🏡✨

Throughout the process, it’s essential to maintain open communication with your mortgage broker and provide them with all the necessary documentation and information. This will help streamline the process and enable your broker to find the best loan options for you. 📄🤝

Preparing for the preapproval process

Before starting the preapproval process, gather all the necessary documentation and information required by your mortgage broker. This includes income statements, bank statements, and other financial documents. By preparing these documents in advance, you can expedite the preapproval process and increase your chances of securing the best mortgage terms. 📑🚀

Additionally, consider getting preapproved for a mortgage from a mortgage broker who has access to compare rates and fees from multiple end investors. This will enable you to find the best mortgage option for your needs and ensure that you are making an informed decision. 🏦💼

Working with a real estate agent

Partnering with a real estate agent during the homebuying process can provide numerous benefits. A knowledgeable real estate agent can help you with:

Finding the perfect property

Negotiating the best price

Guiding you through the mortgage process

Collaborating with your mortgage brokerage to ensure a smooth and efficient process.

To make the most of your partnership with a real estate agent, follow these steps:

Maintain open communication with your agent.

Provide them with all the necessary information about your budget, preferences, and needs.

This will enable your agent to find the best property for you and streamline the mortgage process with your brokerage.

Shopping and Comparing Loan Options

Exploring and comparing various mortgage loan options is essential to finding the best fit for your needs. By working with a mortgage brokerage, you can:

Access a wide range of loan programs and interest rates from multiple lenders

Compare different offers

Select the most competitive mortgage for your financial situation

As you compare loan options, consider factors such as interest rates, fees, and loan terms. By thoroughly evaluating these factors, you can make an informed decision and secure the best mortgage for your needs.

How mortgage brokers shop end investors for you

Mortgage brokers work tirelessly to find the most competitive loan options for you from various end investors, such as banks, credit unions, and other financial institutions. By shopping around and comparing rates, fees, and loan terms from multiple lenders, they can help you secure the best mortgage for your needs. 🏦🔍

Working with a mortgage broker can save you time and effort in the homebuying process. They can provide you with guidance and advice, allowing you to focus on finding the perfect property and preparing for your move.

By trusting your mortgage broker to shop end investors for you, you can ensure that you are getting the best possible mortgage terms and rates. This partnership allows you to navigate the mortgage landscape with confidence and ease! 🌟

In today’s fluctuating mortgage market, using the lock-and-shop strategy can be beneficial. This strategy involves locking in an interest rate with a lender before searching for your new home. By locking in a rate, you can protect yourself from increasing interest rates while shopping for a home with a realtor. 🔒

The benefit of using a lock-and-shop is that it can reduce anxiety in a volatile interest rate environment, especially if you are shopping at the high end of your purchase range and may find yourself otherwise priced out of the market if interest rates increase.

Summary

In conclusion, finding the best mortgage brokerage in 2026 is a crucial step in securing the perfect home loan for your needs. By comparing top mortgage lenders, understanding the importance of credit scores and down payments, navigating the mortgage process with a brokerage, and exploring various loan options, you can make an informed decision and secure the best mortgage terms for your dream home. 🏡✨

Remember, the homebuying journey is an exciting and rewarding process, and working with a mortgage brokerage can make it even more seamless. With the right guidance and persistence, you’ll be well on your way to finding the perfect mortgage and stepping into your dream home.

Frequently Asked Questions

Is it worth paying a mortgage broker?

Working with a mortgage broker may be worth it if they can secure you a better deal than you can get on your own. A broker can save you time by shopping around for the best mortgage, as well as potentially lower fees and interest rates than commercial lenders offer.

Also, consider that the lender who works for the customer’s best interest educates on the pros and cons of the loan programs and builds their business for the long-term benefit of their customers over their own short-term gain will likely be the best bet, even if the interest rate pricing is slightly higher. In that respect, it’s a bit like choosing a lawyer—get the lawyer who wants your best outcome over the lawyer who simply promises the lowest fees.

How much do most mortgage brokers charge?

Mortgage brokers typically charge a loan origination fee that ranges from 0.50% to 2.75% of the loan principal, with most fees falling between 1-2%.

This fee is typically paid at closing and is in addition to other closing costs.

Is it best to talk to a mortgage broker or bank?

If you need help comparing options from multiple lenders, a mortgage broker is the best choice. A bank can be a good option at times, depending on their loan options offering and customer service level.

What are some popular mortgage lenders in 2026?

Popular mortgage lenders in 2026 include Rocket Mortgage, Ally Bank, Fairway Independent Mortgage Corporation, LoanDepot, Mr. Cooper, New American Funding, Flagstar Bank, PNC Bank, Chase, and PenFed. However, you may find a mortgage broker who has access to more loan options, is local, and cares about your long-term financial picture, which is a better option for you.

Buying a home in Colorado can feel daunting, especially when you are trying to save for a down payment, plan for closing costs, and understand what monthly mortgage payment fits your budget.

CHFA loans Colorado homebuyers use are designed to make the homeownership journey more accessible for qualified borrowers. Through the Colorado Housing and Finance Authority (CHFA), eligible buyers may have access to a mortgage loan along with down payment assistance programs that can help reduce upfront costs.

At The Mortgage Architects, we help buyers understand their options in plain English. Whether you are buying your first home, moving into a new home, or exploring whether you may qualify for down payment assistance, we can help you navigate the entire process with a clear plan.

Colorado Housing and Finance Authority: What Is CHFA?

The Colorado Housing and Finance Authority, often called CHFA, was created in 1973 to strengthen Colorado through investments in affordable housing and community development.

CHFA works throughout Colorado to help make homeownership more achievable for qualified low-to-moderate-income borrowers. In addition to home purchase loan programs, CHFA supports affordable rental housing, community development, and businesses across the state.

For homebuyers, CHFA offers mortgage programs, homebuyer education, and down payment assistance through a statewide network of approved lenders. CHFA does not make mortgage loans directly to consumers. Instead, borrowers work with participating lenders, such as The Mortgage Architects, to review eligibility, submit a loan application, and complete the mortgage process.

CHFA Loans: A Path Toward Homeownership

CHFA loans are designed to help qualified Colorado buyers purchase a primary residence with more manageable upfront cash requirements.

A CHFA mortgage may be paired with a conventional, FHA, VA, or USDA-RD first mortgage loan, depending on the buyer’s qualifications and the program available. Some programs are designed specifically for first-time homebuyers, while others may be available to repeat homebuyers who meet program requirements.

The right option depends on several factors, including:

Available funds for your down payment and closing costs

Type of mortgage loan

Whether you are a first-time buyer, repeat buyer, veteran, or may qualify for a specialized CHFA program

A CHFA loan is not automatically the best deal for every borrower. Interest rates, fees, mortgage insurance, and repayment terms can vary by program and loan type. The goal is to compare the full picture—not just the amount of assistance available—so you can make a confident decision for your home purchase.

Down Payment Assistance

One of the biggest barriers to buying a house is saving enough cash for the down payment and closing costs. CHFA down payment assistance programs may help eligible borrowers bridge that gap.

Buyers using a qualifying CHFA first mortgage loan may be able to receive assistance toward their down payment, closing costs, and in some cases prepaid expenses. Even if you are able to contribute money toward your purchase, you may still qualify to use CHFA assistance.

CHFA currently offers two primary down payment assistance options:

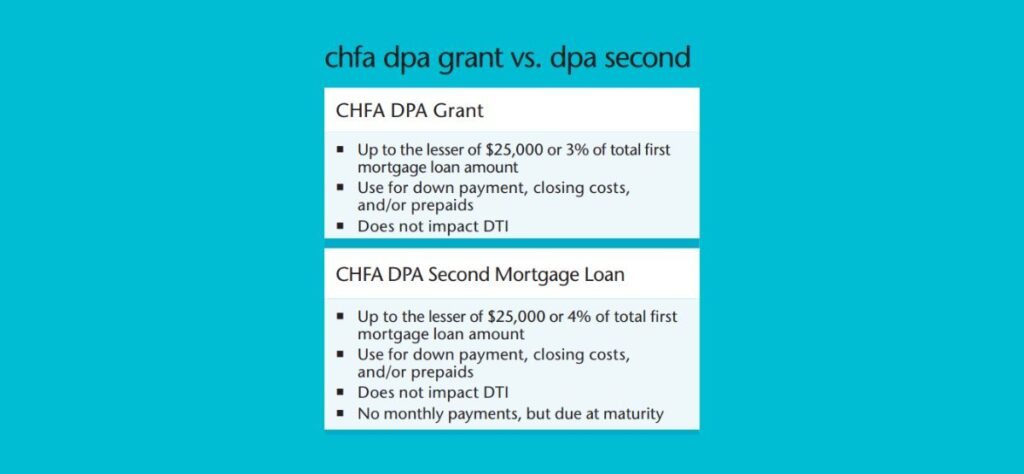

Down Payment Assistance Grant

The CHFA Down Payment Assistance Grant may provide up to the lesser of:

$25,000, or

3% of the first mortgage loan amount

This is a grant, which means no repayment is required when the program terms are met.

For example, on a $300,000 first mortgage loan, 3% would equal $9,000 in potential assistance. Actual eligibility and assistance amounts vary based on the loan program and borrower profile.

Down Payment Assistance Second Mortgage Loan

The CHFA Down Payment Assistance Second Mortgage Loan may provide up to the lesser of:

$25,000, or

4% of the first mortgage loan amount

Unlike the grant, this assistance is a second mortgage loan. Payments are generally deferred, meaning you may not make a monthly payment on it right away. However, the balance typically becomes due when certain events occur, such as paying off the first mortgage loan, selling the home, refinancing, or no longer using the property as your primary residence.

Certain specialized CHFA programs for first-generation homebuyers or individuals living with a permanent disability may offer up to $25,000 regardless of the first mortgage amount.

Down Payment Assistance: Grant vs. Second Mortgage

Both assistance options can help reduce the amount of cash needed at closing, but they work differently.

The CHFA grant may be a fit when: You qualify for an option that does not require repayment and want assistance with your down payment or closing costs.

The CHFA second mortgage may be a fit when: You need a larger amount of assistance and understand that the balance may need to be repaid in the future if you sell, refinance, pay off your first mortgage, or move out of the home.

Because CHFA assistance options may come with higher interest rates on the first mortgage, it is important to compare the total cost of the loan—not just the upfront benefit. Our team can walk through the numbers with you so you understand the payment, interest rates, fees, mortgage insurance, and future repayment obligations before you move forward.

Closing Costs: What Should You Plan to Pay?

Your down payment is only one part of your home purchase budget. Closing costs may include lender fees, title fees, appraisal costs, prepaid taxes and insurance, and other expenses connected with finalizing your mortgage.

CHFA down payment assistance may be used toward eligible closing costs, depending on the program and loan structure. However, buyers should still prepare for expenses that may not be covered.

CHFA generally requires borrowers to make a minimum financial investment of at least $1,000 toward the purchase of the home. This contribution may be counted toward the required down payment or closing costs, depending on the loan terms. Eligible gift funds may also be allowed in some situations.

Before submitting an offer, we help you review a realistic cash-to-close estimate so there are no surprises on closing day.

Who May Qualify for CHFA Loans?

CHFA loans can help first-time homebuyers in Colorado, but some programs may also be available to repeat buyers. Eligibility depends on the program, property, household income, loan type, and lender underwriting requirements.

General CHFA requirements for purchase loans may include:

A mid credit score of 620 or higher for all borrowers, although certain no-credit-score exceptions may be available

Total borrower income that does not exceed applicable CHFA income limits

Completion of a CHFA-approved homebuyer education class before closing

A minimum borrower financial contribution of at least $1,000

Qualification under the underwriting requirements of the participating lender

Purchase of an eligible primary residence in Colorado

Income limits vary by location, household size, program type, and whether the home is located in a federally designated targeted area. In some targeted areas, higher income or purchase price limits may apply.

You do not need to figure this out alone. We can review your income, credit profile, available funds, and homeownership goals to help identify whether CHFA may be worth exploring.

Homebuyer Education for Your Homeownership Journey

CHFA requires borrowers using a CHFA first mortgage loan program to complete a CHFA-approved homebuyer education class before closing.

These classes are available online and in person through approved housing counseling providers throughout Colorado. Taking the class early can help you prepare for the homebuying journey, understand the responsibilities of homeownership, and make better decisions about your budget, mortgage payment, insurance, and long-term costs.

The education requirement is not intended to slow you down. It is a resource designed to help you feel more prepared and protected before making one of the biggest financial decisions of your life.

CHFA Mortgage Options for First-Time and Repeat Buyers

Many people assume CHFA is only for first-time homebuyers. While some programs are specifically designed for buyers purchasing their first home, other CHFA mortgage programs may be available to repeat homebuyers who qualify.

CHFA programs may include options for:

First-time homebuyers

Repeat homebuyers

Veterans using VA financing

Buyers using FHA financing

Eligible USDA-RD borrowers

Buyers purchasing in targeted areas

First-generation homebuyers

Borrowers with a permanent disability or families caring for a qualifying individual

Every program has its own requirements. The best way to understand your options is to compare CHFA with other available mortgage programs, including conventional, FHA, VA, USDA, and non-CHFA assistance opportunities.

Down Payment and Mortgage Insurance

A common question is whether CHFA assistance allows a buyer to avoid mortgage insurance.

The answer depends on the loan program, loan-to-value ratio, and amount of down payment. Mortgage insurance may still be required on many loans when the borrower puts down less than 20%. For conventional loans, this is often called private mortgage insurance, or PMI. FHA loans have mortgage insurance requirements of their own.

Down payment assistance does not automatically eliminate mortgage insurance. However, assistance may help you make a home purchase sooner by reducing the amount of cash you need upfront.

We will help you compare the full monthly payment, including principal, interest, taxes, insurance, and any mortgage insurance, so you know what fits comfortably into your budget.

FAQ

Can You Refinance a CHFA Mortgage?

CHFA refinance options are limited and are generally intended for existing CHFA homeowners with a CHFA FHA first mortgage loan. The CHFA FHA Streamline Refinance program may allow eligible current CHFA FHA borrowers to refinance their first mortgage while keeping an existing CHFA Down Payment Assistance Second Mortgage Loan in place through a one-time subordination, when program requirements are met. If you are considering refinance options, contact us so we can review your existing mortgage, current interest rate, equity, payment, and potential next steps.

Why Work with The Mortgage Architects?

A CHFA loan can be a great resource, but the program details can feel overwhelming. That is where we come in.

The Mortgage Architects is a CHFA participating lender serving Colorado homebuyers, including buyers in Denver and surrounding communities. We help you understand your options, compare loan programs, and build a realistic plan for your purchase.

Our role is to help you:

Understand whether CHFA loans Colorado buyers use may fit your situation

Compare a grant versus a second mortgage for down payment assistance

Review your credit score, income, cash, and monthly payment goals

Estimate down payment and closing costs before you begin house hunting

Navigate lender requirements, paperwork, underwriting, and closing day

Make a confident decision without feeling pressured or judged

You do not need perfect finances, a huge down payment, or all the answers before starting the conversation. You just need a clear picture of where you are and what may be possible.

Partner with a Trusted CHFA Participating Lender

Ready to Explore CHFA Loans in Colorado?

Your dream home may be closer than you think.

Whether you are a first-time buyer, a repeat buyer, or someone who has felt unable to move forward because of down payment concerns, The Mortgage Architects can help you understand your options.

Contact us to schedule a judgment-free consultation. We will review your goals, answer your questions, and help you determine whether CHFA down payment assistance, another Colorado housing program, or a different mortgage loan may be the right path toward homeownership.

Wondering how the NAR verdict changes things for you as a buyer or affects your real estate agent? The ruling not only imposes a $418 million settlement on the National Association of Realtors but also demands a shift in commission structures. In this article, we’ll cut straight to the heart of these changes, exploring how they affect your wallet, your options in the real estate market, and sound advice to protect your home purchase.

What happened— The $418M Settlement

In April 2024, the National Association of Realtors (NAR) agreed to a $418 million settlement. This settlement marks the end of longstanding regulations mandating that home sellers cover the commission costs for both their own broker and the buyer’s broker.

At the heart of the litigation was the practice of tying buyer and seller commissions together, primarily via Multiple Listing Services (MLS). This practice, some argue, has led to stifled competition and escalated fees in the real estate market.

How it will likely shake out for Real Estate Commissions

The verdict against NAR and other real estate organizations may lead to changes in the real estate industry. Some speculate that it will lead to more transparent real estate transactions, which could result in reduced costs for all parties involved.

Increased Disclosures

Real estate agents will provide increased disclosure to their clients regarding compensation options. Additionally, displayed commission rates in online MLS databases may also be eliminated, furthering the push toward transparency in real estate transactions.

Competition Among Agents

The outcome of the antitrust lawsuit signals a potential increase in competition among agents and could lead to the development of a competitive pricing system that enhances service quality and delivers cost savings for consumers.

In the wake of the verdict, rising competition is expected to catalyze innovation and diversification in the services offered by real estate agents. Sellers are now advised to push for reduced commissions, aiming as low as 1.5% for listing agents, further highlighting the shifting dynamics in the real estate industry.

Negotiating Commission Rates

As part of the NAR settlement agreement, preset commission rates and shared commissions between buyers and sellers could be abolished. This move, supported by the trade group, paves the way for more flexible compensation models, giving consumers say in negotiating commission rates.

Tips for Homebuyers and Sellers in the Post-Verdict Market

Navigating the post-NAR verdict market might seem challenging, but understanding the changes and their implications can be empowering. Whether you’re a buyer or a seller, it’s critical to understand the value of a buyer’s agent, the importance of negotiating commission rates, and the evolving dynamics of the real estate market.

Many buyers are questioning whether they need an agent, especially when they might be responsible for the commission. However, a buyer’s agent does more than just show homes—they provide invaluable advice, negotiate on your behalf, and have an expert eye for potential problems in properties that you might overlook.

Expert Guidance

Having a buyer’s agent can be incredibly beneficial, providing expertise and guidance throughout the complex process of buying a home. Market knowledge is another area where buyer’s agents provide unmatched value. They understand local market trends, know what comparable homes are selling for, and can provide insights that help you make informed decisions. This expertise is particularly crucial in a shifting landscape, helping you to navigate the market confidently and successfully.

Negotiating the Best Price

A Buyers Agent can help you negotiate the best price, spot potential issues with a property, and navigate the local market efficiently. In the post-verdict market, the role of buyer’s agents is more critical than ever, and their value cannot be underestimated. In a post-verdict world, where commission structures might change, a buyer’s agent’s negotiation skills are crucial. They’re not just about getting the price down; they also work to secure terms that benefit you, from repair agreements to closing costs. Furthermore, in a competitive market, having an agent who can strategize effectively can make the difference between securing your dream home and missing out.

Largest Purchase with Protections

Would you represent yourself in a major legal battle? Likely not. Purchasing a home is one of the largest financial decisions you’ll make, involving contracts and negotiations that could have long-lasting implications. A skilled buyer’s agent acts as your advocate, ensuring your interests are protected throughout the entire transaction.

Finding Your Real Estate Ally

Choosing the right buyer’s agent is more important than ever. You need someone who is not just knowledgeable but also adaptable to the changes in the real estate industry post-verdict. Look for an agent who understands your needs, has a solid track record, and is committed to representing your best interests.

Remember, a good buyer’s agent will help you see beyond the surface of potential homes, pointing out issues or features you might miss, offering insights into the neighborhood, and providing guidance on the true value of a property. They’re your partner in the home-buying process, offering education and support every step of the way to ensure you make a decision that’s right for you.

In conclusion, despite the evolving landscape, the value of a buyer’s agent remains clear. They are not just facilitators but crucial advisors who can enhance your home-buying experience, provide strategic insights, and help you navigate the complexities of today’s real estate market. In the post-NAR verdict era, having a trusted buyer’s agent by your side is more important than ever.

Negotiating Commission Rates

In the new landscape of real estate, commission rates are no longer preset. While there are standard commission rates in traditional real estate transactions, these are not fixed and can could be negotiated. Factors such as market strength, inventory levels, and the potential for future business can influence an agent’s willingness to negotiate their commission.

While negotiating commission rates is part of the new landscape, the value a skilled agent brings can often exceed the cost of their commission through better deal outcomes, saving money in other aspects of the purchase, or finding the right property more efficiently. It’s worth noting that the rates are often a reflection of the value, expertise, and complexity of the services provided by real estate agents.

In summary, while it’s important to negotiate commission rates, a real estate agent is a highly valuable partner in this complex transaction, and you don’t want to step over dollars to pick up dimes!

Understanding the MLS System

The NAR settlement has sparked significant changes in the MLS system. Commission rates must now be explicitly agreed upon by buyers and their agents, and these rates will no longer be publicly displayed on online MLS databases.

Despite these changes, listing agents retain the ability to communicate buyer’s agent commission through their own websites or directly, maintaining a degree of flexibility in the system. The changes brought about by the NAR agreement could lead to a decline in transparency issues in the MLS system, enhancing buyer awareness of agents’ incentives.

Understanding the changes to the MLS system is crucial for homebuyers and sellers. It’s a new era of transparency and understanding, one that provides consumers with greater control and insight into their real estate transactions.

Summary

The NAR settlement represents a paradigm shift in the real estate industry, disrupting traditional commission structures and ushering in a new era of transparency and fairness. From the abolition of preset commission rates to the rise of competition among agents, the landscape is changing, and it’s essential to stay informed and adapt to these changes.

Frequently Asked Questions

What happened with NAR?

Answer: The National Association of Realtors (NAR) agreed to pay $418 million over four years to resolve all claims against the group by home sellers related to broker commissions. Additionally, NAR agreed to create a new rule prohibiting offers of compensation on the MLS. This agreement is pending court approval.

How can homebuyers and sellers navigate the post-verdict market?

Answer: Understanding the changes in the market and the value of a buyer’s agent can help homebuyers and sellers navigate the post-verdict market effectively. Negotiating commission rates is also important in this process.

How much can I save by using a buyer’s agent who negotiates effectively on my behalf?

Answer: The savings achieved through effective negotiation by a buyer’s agent can be substantial, but they vary based on the property, market conditions, and the specific terms of the deal. A skilled buyer’s agent doesn’t just negotiate the purchase price; they also work on other aspects of the deal, such as closing costs, repair credits, and contingencies, which can all lead to significant savings.

For example, if a buyer’s agent negotiates a $10,000 reduction on the purchase price of a $300,000 home, that’s an immediate 3.3% savings. If they also negotiate for the seller to cover $5,000 in closing costs, the total savings increase. Additionally, by identifying and negotiating repairs or improvements before the sale closes, an agent can save you even more, not just in money but also in future hassle.