Buying a home in Colorado can feel daunting, especially when you are trying to save for a down payment, plan for closing costs, and understand what monthly mortgage payment fits your budget.

CHFA loans Colorado homebuyers use are designed to make the homeownership journey more accessible for qualified borrowers. Through the Colorado Housing and Finance Authority (CHFA), eligible buyers may have access to a mortgage loan along with down payment assistance programs that can help reduce upfront costs.

At The Mortgage Architects, we help buyers understand their options in plain English. Whether you are buying your first home, moving into a new home, or exploring whether you may qualify for down payment assistance, we can help you navigate the entire process with a clear plan.

Colorado Housing and Finance Authority: What Is CHFA?

The Colorado Housing and Finance Authority, often called CHFA, was created in 1973 to strengthen Colorado through investments in affordable housing and community development.

CHFA works throughout Colorado to help make homeownership more achievable for qualified low-to-moderate-income borrowers. In addition to home purchase loan programs, CHFA supports affordable rental housing, community development, and businesses across the state.

For homebuyers, CHFA offers mortgage programs, homebuyer education, and down payment assistance through a statewide network of approved lenders. CHFA does not make mortgage loans directly to consumers. Instead, borrowers work with participating lenders, such as The Mortgage Architects, to review eligibility, submit a loan application, and complete the mortgage process.

CHFA Loans: A Path Toward Homeownership

CHFA loans are designed to help qualified Colorado buyers purchase a primary residence with more manageable upfront cash requirements.

A CHFA mortgage may be paired with a conventional, FHA, VA, or USDA-RD first mortgage loan, depending on the buyer’s qualifications and the program available. Some programs are designed specifically for first-time homebuyers, while others may be available to repeat homebuyers who meet program requirements.

The right option depends on several factors, including:

- Your credit score and mid credit score

- Household income

- Purchase price and property location

- Available funds for your down payment and closing costs

- Type of mortgage loan

- Whether you are a first-time buyer, repeat buyer, veteran, or may qualify for a specialized CHFA program

A CHFA loan is not automatically the best deal for every borrower. Interest rates, fees, mortgage insurance, and repayment terms can vary by program and loan type. The goal is to compare the full picture—not just the amount of assistance available—so you can make a confident decision for your home purchase.

Down Payment Assistance

One of the biggest barriers to buying a house is saving enough cash for the down payment and closing costs. CHFA down payment assistance programs may help eligible borrowers bridge that gap.

Buyers using a qualifying CHFA first mortgage loan may be able to receive assistance toward their down payment, closing costs, and in some cases prepaid expenses. Even if you are able to contribute money toward your purchase, you may still qualify to use CHFA assistance.

CHFA currently offers two primary down payment assistance options:

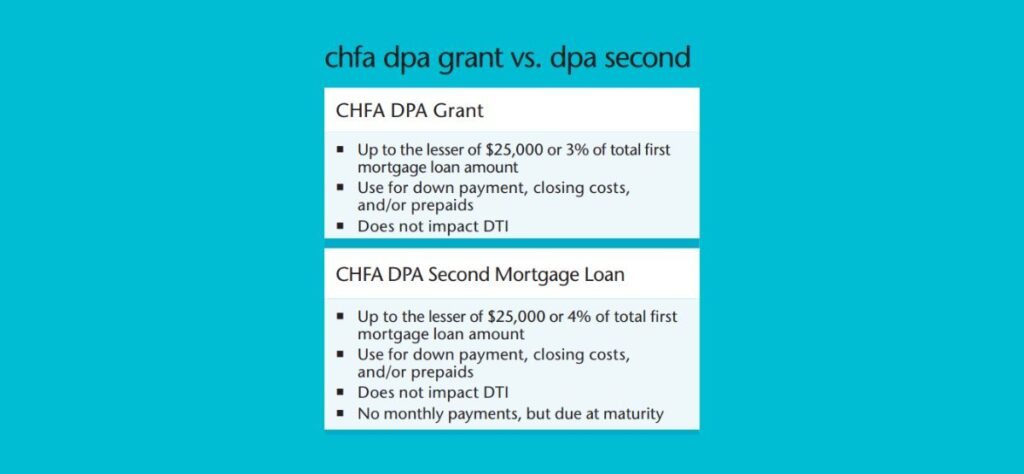

Down Payment Assistance Grant

The CHFA Down Payment Assistance Grant may provide up to the lesser of:

- $25,000, or

- 3% of the first mortgage loan amount

This is a grant, which means no repayment is required when the program terms are met.

For example, on a $300,000 first mortgage loan, 3% would equal $9,000 in potential assistance. Actual eligibility and assistance amounts vary based on the loan program and borrower profile.

Down Payment Assistance Second Mortgage Loan

The CHFA Down Payment Assistance Second Mortgage Loan may provide up to the lesser of:

- $25,000, or

- 4% of the first mortgage loan amount

Unlike the grant, this assistance is a second mortgage loan. Payments are generally deferred, meaning you may not make a monthly payment on it right away. However, the balance typically becomes due when certain events occur, such as paying off the first mortgage loan, selling the home, refinancing, or no longer using the property as your primary residence.

Certain specialized CHFA programs for first-generation homebuyers or individuals living with a permanent disability may offer up to $25,000 regardless of the first mortgage amount.

Down Payment Assistance: Grant vs. Second Mortgage

Both assistance options can help reduce the amount of cash needed at closing, but they work differently.

The CHFA grant may be a fit when:

You qualify for an option that does not require repayment and want assistance with your down payment or closing costs.

The CHFA second mortgage may be a fit when:

You need a larger amount of assistance and understand that the balance may need to be repaid in the future if you sell, refinance, pay off your first mortgage, or move out of the home.

Because CHFA assistance options may come with higher interest rates on the first mortgage, it is important to compare the total cost of the loan—not just the upfront benefit. Our team can walk through the numbers with you so you understand the payment, interest rates, fees, mortgage insurance, and future repayment obligations before you move forward.

Closing Costs: What Should You Plan to Pay?

Your down payment is only one part of your home purchase budget. Closing costs may include lender fees, title fees, appraisal costs, prepaid taxes and insurance, and other expenses connected with finalizing your mortgage.

CHFA down payment assistance may be used toward eligible closing costs, depending on the program and loan structure. However, buyers should still prepare for expenses that may not be covered.

CHFA generally requires borrowers to make a minimum financial investment of at least $1,000 toward the purchase of the home. This contribution may be counted toward the required down payment or closing costs, depending on the loan terms. Eligible gift funds may also be allowed in some situations.

Before submitting an offer, we help you review a realistic cash-to-close estimate so there are no surprises on closing day.

Who May Qualify for CHFA Loans?

CHFA loans can help first-time homebuyers in Colorado, but some programs may also be available to repeat buyers. Eligibility depends on the program, property, household income, loan type, and lender underwriting requirements.

General CHFA requirements for purchase loans may include:

- A mid credit score of 620 or higher for all borrowers, although certain no-credit-score exceptions may be available

- Total borrower income that does not exceed applicable CHFA income limits

- Completion of a CHFA-approved homebuyer education class before closing

- A minimum borrower financial contribution of at least $1,000

- Qualification under the underwriting requirements of the participating lender

- Purchase of an eligible primary residence in Colorado

Income limits vary by location, household size, program type, and whether the home is located in a federally designated targeted area. In some targeted areas, higher income or purchase price limits may apply.

You do not need to figure this out alone. We can review your income, credit profile, available funds, and homeownership goals to help identify whether CHFA may be worth exploring.

Homebuyer Education for Your Homeownership Journey

CHFA requires borrowers using a CHFA first mortgage loan program to complete a CHFA-approved homebuyer education class before closing.

These classes are available online and in person through approved housing counseling providers throughout Colorado. Taking the class early can help you prepare for the homebuying journey, understand the responsibilities of homeownership, and make better decisions about your budget, mortgage payment, insurance, and long-term costs.

The education requirement is not intended to slow you down. It is a resource designed to help you feel more prepared and protected before making one of the biggest financial decisions of your life.

CHFA Mortgage Options for First-Time and Repeat Buyers

Many people assume CHFA is only for first-time homebuyers. While some programs are specifically designed for buyers purchasing their first home, other CHFA mortgage programs may be available to repeat homebuyers who qualify.

CHFA programs may include options for:

- First-time homebuyers

- Repeat homebuyers

- Veterans using VA financing

- Buyers using FHA financing

- Eligible USDA-RD borrowers

- Buyers purchasing in targeted areas

- First-generation homebuyers

- Borrowers with a permanent disability or families caring for a qualifying individual

Every program has its own requirements. The best way to understand your options is to compare CHFA with other available mortgage programs, including conventional, FHA, VA, USDA, and non-CHFA assistance opportunities.

Down Payment and Mortgage Insurance

A common question is whether CHFA assistance allows a buyer to avoid mortgage insurance.

The answer depends on the loan program, loan-to-value ratio, and amount of down payment. Mortgage insurance may still be required on many loans when the borrower puts down less than 20%. For conventional loans, this is often called private mortgage insurance, or PMI. FHA loans have mortgage insurance requirements of their own.

Down payment assistance does not automatically eliminate mortgage insurance. However, assistance may help you make a home purchase sooner by reducing the amount of cash you need upfront.

We will help you compare the full monthly payment, including principal, interest, taxes, insurance, and any mortgage insurance, so you know what fits comfortably into your budget.

FAQ

CHFA refinance options are limited and are generally intended for existing CHFA homeowners with a CHFA FHA first mortgage loan.

The CHFA FHA Streamline Refinance program may allow eligible current CHFA FHA borrowers to refinance their first mortgage while keeping an existing CHFA Down Payment Assistance Second Mortgage Loan in place through a one-time subordination, when program requirements are met.

If you are considering refinance options, contact us so we can review your existing mortgage, current interest rate, equity, payment, and potential next steps.

Why Work with The Mortgage Architects?

A CHFA loan can be a great resource, but the program details can feel overwhelming. That is where we come in.

The Mortgage Architects is a CHFA participating lender serving Colorado homebuyers, including buyers in Denver and surrounding communities. We help you understand your options, compare loan programs, and build a realistic plan for your purchase.

Our role is to help you:

- Understand whether CHFA loans Colorado buyers use may fit your situation

- Compare a grant versus a second mortgage for down payment assistance

- Review your credit score, income, cash, and monthly payment goals

- Estimate down payment and closing costs before you begin house hunting

- Navigate lender requirements, paperwork, underwriting, and closing day

- Make a confident decision without feeling pressured or judged

You do not need perfect finances, a huge down payment, or all the answers before starting the conversation. You just need a clear picture of where you are and what may be possible.

Ready to Explore CHFA Loans in Colorado?

Your dream home may be closer than you think.

Whether you are a first-time buyer, a repeat buyer, or someone who has felt unable to move forward because of down payment concerns, The Mortgage Architects can help you understand your options.

Contact us to schedule a judgment-free consultation. We will review your goals, answer your questions, and help you determine whether CHFA down payment assistance, another Colorado housing program, or a different mortgage loan may be the right path toward homeownership.