When buying or refinancing a home, one of the biggest questions is whether to work with a mortgage broker or go directly to a lender. Here are the most common FAQs to help you decide.

What does a mortgage broker do?

A mortgage broker acts as your personal guide through the loan process. Instead of being tied to one bank, brokers shop multiple lenders to find the best rates and programs for your situation.

How is a mortgage broker different from a lender?

A lender provides loans directly and only offers its own products. A broker works with many lenders, giving you more options and the ability to compare rates and terms in one place.

What are the benefits of using a broker?

Access to more loan programs and competitive rates. Time savings since brokers handle the shopping and paperwork. Potential cost savings — research shows borrowers may save around $9,000 over five years by using a broker.

Are there any drawbacks?

Some brokers may charge fees, and not every lender works with brokers. Still, many borrowers find the wider access to loan options outweighs these limitations.

How do I choose the right broker?

Look for licensed professionals with strong reviews, transparent communication, and experience in your state. A trusted broker should explain all options clearly and align with your financial goals.

✅ Bottom Line

Working with a mortgage broker often means more choices, better rates, and less hassle.

What if you could make a cash offer without having hundreds of thousands of dollars sitting in your bank account? Enter the Cash Offer Loan Program.

This unique program gives everyday buyers the competitive edge of a cash offer, making it easier to win bidding wars, negotiate better deals, and close faster—even with as little as 5% down.

Let’s break down how it works, who it’s for, and why it could be the smartest move in today’s housing market.

“Cash offers bring a much greater level of certainty to the table. Sellers know loans can fall apart—but cash is guaranteed to close.”

And the data backs that up. A University of California San Diego study found that cash buyers pay around 12% less on average than those using traditional financing. That’s a huge savings on a $500,000 home—up to $60,000!

Why do sellers prefer cash?

Speed: Cash deals can close in as little as 10 days.

Certainty: No waiting on lender approvals or appraisals.

Leverage: Sellers will often accept lower offers just to avoid the uncertainty of financing.

Who Is This Program For?

This isn’t just for the wealthy. In fact, it’s designed specifically for buyers who don’t have hundreds of thousands in liquid cash but still want to compete like they do.

Here are a few ideal candidates:

1. First-Time Homebuyers

Trying to buy your first home in a hot market can feel like you’re constantly losing out to investors or wealthier buyers.

“We can now level the playing field for first-time buyers. You don’t need perfect credit or a massive down payment,” says Jennison.

Minimum credit score: 640

Down payment as low as 5%

Close in as little as 10 days

2. Move-Up Buyers

Already own a home, but trying to secure your next one before selling? The Cash Offer Loan lets you buy first—without needing to rush the sale of your current home.

3. Buyers in Competitive Markets

In cities where homes get multiple offers within days, making a traditional offer often just isn’t enough.

“You’re spending around $10,000 on the program, but saving up to $30,000 or more by getting your offer accepted and negotiating a better deal,” Jennison explains.

Use the cash loan to make a strong, non-contingent offer—just like an investor.

Step 3: Win the House

Your cash offer gives you a much higher chance of acceptance, especially in competitive bidding situations.

Step 4: Close in 10 Days

Once the seller accepts, you can close in as little as 10 days.

Step 5: Refinance

After closing, Mortgage Architects quickly works to refinance you out of the short-term loan into a traditional mortgage.

“We’re working to refinance you as quickly as possible—sometimes in just 21 days,” says Jennison.

What Does It Cost?

Yes, this program has fees—but the potential savings far outweigh the costs. Here’s an example based on a $500,000 home:

Program Costs:

5% down payment: $25,000

10% interest (short-term loan): $2,730 for 21 days

Origination fee:

1.5% if putting 5% down ($7,125)

1% if putting 10% down ($4,750)

Total Direct Costs: ~$9,855 (max scenario)

Now compare that to the potential savings of 6–12% on the purchase price:

6% savings on $500,000 = $30,000

Even after fees, you come out $20,000 ahead

“It’s a 3:1 return on your investment. That’s really strong,” says Jennison.

Why This Program Matters Right Now

With low inventory and high buyer demand, sellers are calling the shots. That means speed, certainty, and leverage are more important than ever.

The Cash Offer Loan Program lets regular buyers:

Compete with investors and wealthy cash buyers

Win bidding wars more often

Negotiate better purchase prices

Avoid costly contingencies

And best of all? You don’t need perfect credit or massive savings to do it.

“This is one more way Mortgage Architects helps you win—by giving you the tools, strategy, and support to make smarter, faster, and stronger offers,” says Jennison.

Is the Cash Offer Loan Right for You?

If you’ve been struggling to get your offer accepted, losing to cash buyers, or want to avoid overpaying in a bidding war—this program might be exactly what you need.

✅ Great for first-time buyers ✅ Ideal for competitive markets ✅ Smart for move-up buyers ✅ Works with 640+ credit ✅ Only 5% down required

Next Steps: Let’s Get You Pre-Approved

Ready to stand out in the market and finally win the home of your dreams?

Reach out to Nathan Jennison and the team at Mortgage Architects to get pre-approved for the Cash Offer Loan Program. You’ll gain a competitive edge and unlock the power of cash—without needing to be a millionaire.

👉 Contact us today and let’s get started. Your dream home might be one winning offer away.

Without an equity bridge loan, buying a new home while still owning your current one can feel like trying to leap across a canyon without a bridge. You need access to your home equity for a down payment—but you can’t access it until you sell.

If that’s your situation, you’re not alone. Many families are stuck in this tricky transition. That’s where the Instant Equity Bridge Loan becomes a lifeline.

This smart solution helps you unlock your equity early, so you can make a non-contingent offer on your next home—and move forward with confidence.

A Real-Life Scenario: The Martins’ Home Buying Dilemma

Let’s imagine the Martins—a growing family of five. Their current home served them well when the kids were little, but now it’s tight. Sharing bedrooms and limited storage is taking a toll on everyone.

They find a perfect new home: more space, a better school district, and a backyard made for summer BBQs. But like many families, their equity is tied up in their current home, and they don’t have the funds available for a down payment—yet.

Every offer they submit must be contingent on selling their home first, and in a competitive market, that puts them at a serious disadvantage.

That’s when they discover the Equity Bridge Loan.

Why Contingent Offers Are Risky

In today’s fast-paced real estate environment, sellers aren’t keen on waiting.

Sellers are much more likely to take a non-contingent offer, even if it’s for a lower price,” says Nathan Jennison of The Mortgage Architects. “That’s why we created a program to help buyers unlock the equity in their existing home before they sell.”

The Martins used the Equity Bridge Loan to tap into their home equity before listing their house, making them non-contingent buyers with strong offers.

What is an Equity Bridge Loan?

An equity bridge loan lets you borrow against the equity in your current home before you sell it. This gives you the cash you need for the down payment and closing costs on a new home—without waiting for your old home to sell.

Key Features:

No monthly payments required

Access equity from a listed or unlisted property

Use alongside other programs like the Guaranteed Backup Contract

Strengthen your purchase offers and speed up your timeline

How the Process Works

Here’s how you can make your move seamless with an equity bridge loan:

Get Pre-Approved First, you’ll get pre-approved for your new mortgage and the equity bridge loan with The Mortgage Architects.

Shop Without Contingencies You’re now ready to make non-contingent offers that stand out in a seller’s market.

Close on the Bridge Loan About 4 days before your new home purchase, the bridge loan is funded—giving you the cash needed to close.

Move In First, Sell After You move into your new home, then list your previous home for sale without the pressure of a rushed timeline.

Pay Off the Bridge Loan at Sale When your current home sells, the proceeds pay off the bridge loan—done and done.

How Much Does It Cost?

Let’s walk through a typical example for a $200,000 equity bridge loan:

Cost Breakdown:

Lender Fee:

2% (if in first position) = $4,000

2.5% (if in second position) = $5,000

Interest:

10% annual rate

About $1,642 for 30 days

Origination Fee:

Waived if The Mortgage Architects handles your purchase mortgage

Otherwise, 1% ($2,000 on $200,000)

Estimated Total:

$5,642 – $8,642, depending on loan position and timing.

While this isn’t a free service, it’s often a small price to pay to avoid losing your dream home or carrying double housing costs from moving into temporary lodging.

Equity Bridge Loan Frequently Asked Questions

What types of homes qualify?

Your current home can be:

Listed

Unlisted

Under contract This program is flexible.

Are there monthly payments?

No monthly payments are required. Interest accrues and is paid off when your current home sells.

How long can I keep the loan?

This is meant to be a short-term loan—typically used for 30–90 days.

Can I use this with other offers?

Yes! Pair it with:

Guaranteed Backup Contract

Cash Offer Loan Program These combinations help you negotiate from the strongest possible position.

Why This Matters: The Martins’ Win

With their bridge loan in place, the Martins made a strong offer on the perfect home—and won. They moved in stress-free, then listed their previous home once they were comfortably settled.

Thanks to the Instant Equity Bridge Loan:

✅ They didn’t have to move twice ✅ They avoided contingent offers ✅ They accessed their equity when they needed it most

Final Thoughts from Nathan Jennison

“This is another way The Mortgage Architects help you move forward. We help you negotiate from a stronger position and transition homes in a way that’s convenient and cost-effective.”

If you’re caught in the in-between of buying and selling, the Equity Bridge Loan might be the smartest step you take.

Making a non-contingent offer in today’s competitive housing market can be the difference between winning your dream home—or losing out to a more prepared buyer.

If you’re a homeowner who wants to buy a new home before selling your current one, but aren’t sure how to manage the financial overlap, there’s a strategic solution that allows you to move forward without making your offer contingent on a home sale.

It’s called a Non-Contingent Guaranteed Backup Contract, and it’s giving buyers more control, flexibility, and buying power.

A Hypothetical Scenario: How the Thompson Family Could Benefit

Imagine a family—let’s call them the Thompsons—who’ve outgrown their starter home. With two kids and a dog, they’re ready to upgrade to a larger home with a yard and better school district.

The catch? They can’t qualify for a new mortgage while still carrying their current one. Listing their home before buying feels risky, and they don’t want to miss out on a great new property.

This is where a non-contingent offer using the Guaranteed Backup Contract comes in. It allows the Thompsons to move forward with confidence, knowing they have a fallback plan if their home doesn’t sell in time.

“This program is designed to give families like the Thompsons the peace of mind and flexibility they need. You can move forward without being contingent on selling first, and that makes all the difference in today’s fast-moving market.” – Nathan Jennison, Mortgage Architects

What Is a Non-Contingent Guaranteed Backup Contract?

It may sound complex, but it’s surprisingly straightforward.

How It Works:

It’s a simple purchase contract placed on your current (departing) residence.

This contract lets you make a non-contingent offer on a new home.

It improves your debt-to-income ratio, making it easier to qualify.

You get up to 120 days post-purchase to sell your existing home.

A lender guarantees to buy your home if it doesn’t sell, protecting your transaction.

Why It Works: Backed by Fannie Mae Guidelines

This program isn’t just clever financing—it’s backed by Fannie Mae. Here’s why that matters:

With a signed, executed contract on your current home, lenders can exclude that mortgage from your debt-to-income ratio.

This dramatically increases your ability to qualify for a new mortgage.

The program has been structured to meet Fannie Mae standards, offering legitimacy and security.

Cost Breakdown: Affordable Peace of Mind

You might expect a program like this to come with a hefty price tag. But the cost is surprisingly reasonable.

Flat Fee: $2,500

Minimum Down Payment: 5% (for a conventional loan)

Other Fees: Standard loan closing costs still apply

For just $2,500, you unlock the ability to make a strong, non-contingent offer and reduce the financial stress of juggling two properties.

Who Should Consider a Non-Contingent Offer?

This strategy is ideal for homeowners in several common scenarios:

You Should Consider It If:

Your home is listed or under contract, but the buyer backs out last minute.

You’ve found your dream home but haven’t sold your current one.

You want to make a stronger, more competitive offer.

Your debt-to-income ratio is too high with both mortgages included.

What’s the Catch? Worst Case Scenario Explained

Every program has its fine print, and this one is no exception.

The lender’s offer will be around 78% of your home’s estimated market value, based on an automated valuation model.

If the home doesn’t sell within 120 days, you can request an extension—but the absolute deadline is 180 days.

If the lender buys the home:

They’ll use your original listing agent to resell it.

90% of the net profit (after costs) from the resale goes back to you.

This protects you from major losses, and ensures the lender has no interest in profiting from your property—they just want to ensure the deal can close.

“This lender isn’t in the business of buying homes—they’re offering a guarantee to protect you. In most cases, they never have to buy the property at all.” – Nathan Jennison

Program Limitations to Keep in Mind

Before moving forward, it’s important to know:

This program is only available for conventional loans.

It does not work with FHA, VA, or USDA loans.

However, for buyers using conventional financing, it’s a game-changer.

Combine It with Other Mortgage Solutions

This isn’t a standalone tool—you can layer it with other programs for maximum benefit:

This gives you the flexibility to create a financing strategy that fits your exact situation.

Final Thoughts: Empower Your Next Move with a Non-Contingent Strategy

A non-contingent offer gives you leverage in a hot market, reduces stress, and provides peace of mind that your current home will sell—or be backed by a lender if it doesn’t.

If you’re ready to buy your next home and want to avoid the typical pitfalls of buying before you sell, reach out to Nathan Jennison and his five star team at The Mortgage Architects to explore your options.

“At the end of the day, it’s about giving you options. You don’t have to feel stuck. This program helps you move forward confidently—whether you’re upsizing, downsizing, or just making your next move.” – Nathan Jennison

If you’re a non-permanent resident dreaming of owning a home, or if you’re considering refinancing your current FHA loan, big changes are coming your way. As of May 25th, the Federal Housing Administration (FHA) will stop insuring loans for non-permanent residents. This shift, aligned with prior Trump-era immigration policies, could drastically alter your home financing options—unless you act now.

In this article, we’ll break down what’s happening, why it’s changing, and most importantly—what you can do to stay on track with your homeownership goals.

What’s Changing With FHA Loans?

Starting May 25th, non-permanent residents will no longer be eligible for FHA loans. While you can still close on an FHA loan after that date, your loan must be under contract and have an FHA case number assigned before May 25th to qualify under the current guidelines.

This is not a permanent ban on all loans for non-permanent residents—but it does significantly reduce accessible options, especially for those who rely on FHA’s flexible credit and income requirements.

Why Is the FHA Making This Change?

The FHA insures home loans through the U.S. government. Because of this backing, it’s seen as a federal benefit. With concerns around the risk of loan default tied to deportation, the FHA is tightening its eligibility guidelines.

This change reflects a more restrictive approach to immigration-related benefits and is seen as a risk management move by the federal government.

Who Will Be Most Affected?

Approximately 10 million non-permanent residents in the U.S. may feel the impact of this change. FHA loans are often the go-to option for:

Buyers with credit scores below 700

Borrowers with higher debt-to-income ratios

First-time homebuyers using down payment assistance programs (DPAs)

With FHA loans off the table, many buyers will need to shift to conventional loan options, which often have stricter qualification criteria.

What Are the Alternatives to FHA Loans?

Good news: FHA loans aren’t the only game in town.

✅ Conventional Loans

Fannie Mae and Freddie Mac have not (yet) followed the FHA’s lead on non-permanent resident eligibility. This means:

First-time homebuyers may qualify with as little as 3% down—if they have a credit score of 700+

There are conventional DPA programs still available, like Colorado’s CHFA

✅ Non-Agency Lenders

Some non-agency lenders (private institutions) are not making any changes. These lenders may still offer financing for non-permanent residents, but expect:

Higher down payments (typically 10–15% minimum)

Possibly higher interest rates

These lenders can be a solid option if you don’t meet conventional guidelines but need to move quickly.

What Should You Do Next?

🏡 If You’re Buying a Home:

Get pre-approved ASAP if you’re a non-permanent resident planning to use an FHA loan.

You must be under contract and have a case number issued before May 25th to qualify.

Act now to lock in lower down payment options and access to FHA’s more lenient requirements.

🔄 If You’re Refinancing:

Already have an FHA loan but credit below 700?

Now may be the time to refinance, before you’re no longer eligible.

Reach out to your loan officer to discuss whether this is the right move.

Credit Score Is Key to Lower Down Payments

If you’re a non-permanent resident and your credit score is close to 700, now is the time to focus on boosting it.

With a score in the 700s, you can access 3% down options through conventional loans.

Improving your credit could mean thousands saved in upfront costs.

Don’t Panic—Plan Instead

This policy change is significant, but it doesn’t have to derail your homeownership journey. What matters most is planning ahead and knowing your options.

Key Takeaways:

FHA loans will not be available to non-permanent residents after May 25th

You must be under contract with an assigned case number by that date to qualify

Alternatives include conventional loans and private lenders

Boost your credit score to access better options

Refinance now if you already have an FHA loan and won’t qualify for other options soon

Final Thoughts

“There’s a lot of fear out there. This isn’t the end of the road,” says Nathan Jennison, Managing Broker and Owner of Mortgage Architects. “It’s about making intelligent, informed plans so you can still achieve your homeownership goals.”

Whether you’re buying or refinancing, time is of the essence. Connect with your real estate agent and mortgage professional today to map out your strategy.

Frequently Asked Questions: FHA Loan Changes for Non-Permanent Residents

1. What exactly is changing with FHA loans?

As of May 25, 2025, non-permanent residents will no longer be eligible for FHA-insured loans. This includes new home purchases and refinances. To qualify under current guidelines, borrowers must have an FHA case number assigned before May 25th.

2. Can I still close on my FHA loan after May 25th?

Yes—as long as your loan is under contract and your FHA case number has been assigned prior to May 25th, you can still proceed with closing after that date.

3. Why is this policy change happening?

The FHA is aligning with federal immigration policies, aiming to reduce risk associated with loan defaults due to potential deportations. Since FHA loans are backed by the U.S. government, they are viewed as a form of public benefit.

4. Are conventional loans still available for non-permanent residents?

Yes—for now. Fannie Mae and Freddie Mac have not announced similar restrictions, so conventional loans remain an option, especially for borrowers with credit scores of 700 or higher.

5. What other loan options do I have if I’m a non-permanent resident?

Beyond FHA and conventional loans, private or non-agency lenders still offer mortgage products. These typically require:

10–15% down payment

Higher credit scores

Possibly higher interest rates

6. I already have an FHA loan—should I refinance now?

If you are a non-permanent resident with an FHA loan and don’t anticipate your credit score reaching 700+, it may be wise to refinance now before the policy change takes effect.

7. What if I need down payment assistance?

Most down payment assistance (DPA) programs are tied to FHA loans, but some states (like Colorado’s CHFA) offer conventional-based DPAs that remain available.

8. How do I boost my credit to qualify for a conventional loan?

To reach the 700+ credit score range:

Pay down high credit card balances

Make on-time payments

Avoid opening new credit lines

Work with a credit advisor if needed

9. I’m not sure which loan type I qualify for—what should I do?

Start by getting pre-approved. A mortgage professional can assess your unique situation and help you identify the best loan type for your goals.

10. Who should I contact to get started before May 25th?

Contact Nathan Jennison and the team at Mortgage Architects as soon as possible. Timing is critical to preserve your FHA eligibility.

The home buying process brings with it one of the biggest financial decisions you’ll ever make. It can be an exciting journey, but also one filled with uncertainty and anxiety if you’re not prepared. Understanding the process can help reduce stress and ensure that you make the best choices for your future.

In this guide, we’ll walk through the essential steps of buying a home, from selecting the right team to celebrating your new purchase. Let’s dive in!

Step 1: Select Your Real Estate Team

Your home-buying journey starts with choosing the right real estate agent and lender. This is crucial because these professionals will guide you through every step of the process.

How to Choose the Right Real Estate Agent and Lender:

Do Your Research: Read reviews and ask for recommendations.

Avoid Choosing Based on Familiarity: Don’t select a lender or agent just because they are a friend or family member.

Look for Experience: Choose professionals who have a strong track record in your desired location.

Ensure They Work for Your Best Interest: A good agent will negotiate well for you, while a trustworthy lender will provide honest and transparent information.

🔑 Pro Tip: Many lenders are predatory, meaning they may not disclose all details upfront. Choose someone who educates you throughout the process and aligns with your financial goals.

Step 2: Get Pre-Approved (Not Just Pre-Qualified!)

Pre-approval is a critical step before you start house hunting. It shows sellers that you’re a serious buyer and strengthens your offer.

Pre-Approval vs. Pre-Qualification:

Pre-Qualification: A lender pulls your credit and takes your word on income and debts—NOT very reliable.

Pre-Approval: A lender verifies your documents, runs financial algorithms, and provides a more accurate borrowing limit.

💡 Why It Matters: Sellers take offers with pre-approvals more seriously because they know the buyer is financially ready.

Allow at least one week for pre-approval to ensure all necessary verifications are completed.

Step 3: House Hunting & Making an Offer

Once you have your pre-approval, the fun part begins—house hunting!

Tips for a Successful Home Search:

Create a must-have list (location, size, amenities).

Be open to compromises but stay within your budget.

Rely on your agent’s expertise to navigate the market.

Once you find the right home, your agent will help negotiate the best price and terms.

Step 4: Get Under Contract & Lock in Your Interest Rate

After your offer is accepted, it’s time to:

Get under contract – The seller agrees to your terms.

Lock in your interest rate – This ensures that the rate you qualify for won’t change before closing.

Choosing the Right Interest Rate:

Ask if you’ll need to pay points (an upfront cost to lower your rate).

Make sure your lender explains all rate options to you.

Consider how long you’ll stay in the home before paying points.

🏡 Your Goal: Secure a rate that fits your financial plans, not just what benefits the lender.

Step 5: Review Loan Disclosures

Once under contract, your lender will send you disclosures outlining the terms of your loan.

Key Points to Know:

These disclosures are not a final obligation to take the loan.

They allow you to review and understand the terms.

If something looks off, ask questions!

📝 Action Item: Review the disclosures carefully and clarify anything unclear with your lender.

Step 6: Home Inspection & Renegotiation

A third-party home inspector will examine the property and identify any issues.

You can renegotiate with the seller for repairs or a lower price.

If serious issues arise, you may have the option to exit the contract without losing your deposit.

🛠️ Pro Tip: Never skip a home inspection! It’s your best chance to avoid expensive surprises later.

Step 7: Home Appraisal (If Required)

The lender usually requires an appraisal to ensure the home is worth what you’re paying.

What Happens During an Appraisal?

A licensed appraiser evaluates the property.

They compare it to recent sales of similar homes.

The lender bases the loan on the lower of the purchase price or appraised value.

If the home appraises lower than your offer, you may need to:

Negotiate a lower purchase price.

Pay the difference out of pocket.

Challenge the appraisal if it seems inaccurate.

📊 Why It’s Important: The appraisal protects both you and the lender from overpaying.

Step 8: Loan Underwriting & Conditional Approval

The lender’s underwriter will review all documents to ensure the loan meets requirements.

Possible Conditions the Lender May Ask For:

Additional income verification.

Proof of funds for closing.

Clarifications on credit history.

📌 Action Item: Respond quickly to any lender requests to avoid closing delays.

Step 9: Clear to Close & Final Preparations

Once your loan is fully approved, you receive a clear to close—this means everything is in place for your final signing!

Key Final Steps:

The lender finalizes the loan documents.

The title company balances the final figures.

You receive final closing costs and payment instructions.

🚨 Beware of Wire Fraud: Only send your down payment and closing costs after verifying wire instructions directly with the title company over the phone.

Step 10: Closing Day – Sign & Celebrate!

Closing day is here! 🏡🎉

What to Expect at Closing:

You’ll sign multiple documents related to your mortgage.

The seller transfers ownership.

Your lender funds the loan.

You receive keys to your new home!

Before signing, do a final walkthrough to ensure the property is in the expected condition.

📌 Pro Tip: Stretch your wrist beforehand—you’ll be signing a lot of papers!

Final Step: Celebrate Your New Home! 🎉

Congratulations! You are now a homeowner. Before jumping into moving and unpacking, take a moment to celebrate your achievement.

Ways to Celebrate:

✅ Host a small gathering. ✅ Pop some champagne! 🍾 ✅ Take a photo in front of your new home. ✅ Share the news with family & friends.

You worked hard for this—don’t skip the celebration!

Final Thoughts: Make Your Home Buying Experience Smooth

By following these steps, you can reduce stress and avoid surprises during the home buying process.

Key Takeaways:

Choose experienced professionals for your team.

Always get pre-approved, not just pre-qualified.

Understand all your loan terms and interest rates.

Use the inspection and appraisal to protect your investment.

Be aware of potential scams, especially wire fraud.

Enjoy and celebrate your success!

If you have more questions about the home-buying process, feel free to reach out. Happy house hunting! 🏡🔑

Home Buying Process Frequently Asked Questions

1. What is the first step in buying a home?

The first step is selecting your real estate team, including a knowledgeable real estate agent and a trustworthy lender. These professionals will guide you through the process and help you make informed decisions.

2. What is the difference between pre-qualification and pre-approval?

Pre-qualification is a basic review of your credit and self-reported finances.

Pre-approval involves submitting financial documents and getting verified, making you a stronger buyer in the eyes of sellers.

3. Why is pre-approval important?

It gives sellers confidence that you can secure financing, making your offer more competitive. It also helps you understand your budget.

4. When should I lock in my interest rate?

Once you are under contract, work with your lender to determine the best time to lock your rate, ensuring you get a favorable and predictable mortgage payment.

5. What is a home inspection, and why is it necessary?

A home inspection is a professional evaluation of the property’s condition, helping you identify potential issues before finalizing your purchase.

6. Can I negotiate after the home inspection?

Yes! If significant issues are found, you can negotiate repairs, request a price reduction, or even walk away from the contract.

7. What is a home appraisal, and how does it impact my loan?

A home appraisal determines the market value of the property. If the appraisal is lower than the purchase price, you may need to renegotiate the price or cover the difference.

8. What happens during the underwriting process?

The lender reviews all financial documents and conditions before giving the final loan approval. Be prepared to submit additional paperwork if requested.

9. What does “clear to close” mean?

It means your loan has been fully approved, and you’re ready to move forward with signing the closing documents.

10. How do I protect myself from wire fraud when making my down payment?

Always call the title company directly to verify wire instructions before sending any funds. Do not rely on email instructions alone.

11. What happens on closing day?

You’ll sign multiple documents, pay any required closing costs, and officially take ownership of your new home. A final walkthrough is also recommended before signing.

12. When can I move into my new home?

Typically, you can move in once the transaction is recorded, which is usually the same day or shortly after closing.

Home title theft is a rare but serious crime that is gaining more attention. While you shouldn’t be overly worried, being aware of how it happens and how to protect yourself is essential. Scammers are finding new ways to steal property ownership, which can lead to financial and legal headaches.

Let’s break down what home title theft is, how scammers pull it off, and the steps you can take to safeguard your home.

What Is Home Title Theft?

Home title theft occurs when fraudsters obtain your personal information and forge documents to transfer ownership of your home into their name. Once they appear as the “new owner,” they can:

While this crime is still relatively rare, the increasing number of online data breaches and sophisticated fraud tactics make it a growing concern.

How Does Home Title Theft Happen?

Scammers use various tactics to steal your home title, often relying on stolen personal information. Here’s how they do it:

Step 1: Stealing Your Personal Information

Fraudsters need details like your Social Security number, birthdate, and other sensitive data. They obtain this information through:

Phishing emails pretending to be from banks or government agencies

Data breaches that expose your private information

Stealing mail from your mailbox that contains sensitive documents

Step 2: Forging Property Documents

Once they have your information, scammers create fake documents such as:

A forged warranty deed or quitclaim deed to transfer ownership

Faked notarization by either forging a notary’s signature or bribing a legitimate notary

Step 3: Recording the Fake Documents

After forging the documents, the scammer files them with the county recorder’s office, making it appear as if they are the rightful owner.

Step 4: Accessing Your Home’s Equity

Now that they have control of the title, fraudsters can:

Take out a cash-out refinance or HELOC using your home’s value

Attempt to sell the property to an unsuspecting buyer

While they don’t legally own your home, the fraud can cause legal trouble and financial losses for the true owner.

Warning Signs of Home Title Theft

Since home title theft happens quietly, it’s important to recognize red flags that could indicate something is wrong:

✅ Receiving new loan statements in the mail – If you get a notice for a mortgage or home loan you didn’t take out, investigate immediately.

✅ Unexpected credit notifications – If you receive a notification about new credit accounts in your name, scammers may be using your identity.

✅ Missing mail – If your mail suddenly stops arriving, scammers may have changed your mailing address to prevent you from receiving warnings.

✅ Notice from the county clerk – If you get a notification about a change in property ownership, take it seriously and verify it.

✅ Strange calls or letters – Be cautious of calls or letters regarding financial matters related to your property that you didn’t initiate.

How to Protect Yourself from Home Title Theft

While this crime is rare, taking proactive steps can reduce your risk significantly. Here’s how you can protect yourself:

1. Freeze Your Credit

A credit freeze prevents scammers from opening fraudulent accounts in your name. You can request a credit freeze from the three major credit bureaus:

TransUnion

Equifax

Experian

Once your credit is frozen, lenders cannot approve new loans using your identity.

2. Get Homeowner’s Title Insurance

Homeowner’s title insurance is a one-time purchase that protects you from fraudulent claims on your property title.

If someone claims ownership of your home before you purchased it, title insurance covers the cost of legal defense.

If you’re buying a home, always ensure the title is clean and clear before closing the deal.

3. Monitor Your Credit and Property Records

Regularly check your credit reports and property title records to ensure there are no unexpected changes.

Check your credit report annually – You are entitled to one free credit report per year from each bureau.

Monitor your county recorder’s office – Some counties allow homeowners to sign up for alerts when their property title is changed.

4. Be Careful with Your Mail

Mail theft is one of the easiest ways for scammers to steal your information. Protect yourself by:

Using a locked mailbox to prevent theft

Opting for paperless statements from banks and lenders

Shredding documents containing sensitive personal information before disposing of them

5. Verify Any Suspicious Communications

If you receive a letter, email, or phone call about your home’s title or finances:

Never call numbers listed in emails or letters – Instead, contact banks and county offices directly using official numbers from their websites.

Be wary of phishing scams – Avoid clicking links in emails claiming to be from financial institutions.

What to Do If You’re a Victim of Home Title Theft

If you suspect your home title has been stolen, take immediate action:

1️⃣ Contact your county recorder’s office – Inform them about the fraudulent documents and request an investigation. 2️⃣ Report identity theft – File a report with the Federal Trade Commission (FTC) at www.IdentityTheft.gov. 3️⃣ Freeze your credit – Contact Experian, TransUnion, and Equifax to lock your credit. 4️⃣ Hire a real estate attorney – A legal expert can help you regain control of your property title. 5️⃣ Alert your mortgage lender – Notify your bank or mortgage company to prevent unauthorized transactions.

Final Thoughts: Stay Vigilant, Stay Protected

Home title theft is rare but serious. The good news is that you can take steps to protect yourself. Freezing your credit, monitoring your records, and securing title insurance are some of the best ways to prevent fraud.

If you ever suspect suspicious activity related to your home, act quickly to limit the damage. Your home is one of your biggest assets—keeping it safe should always be a priority.

If you have any questions or need guidance, feel free to reach out—we’re here to help!

Would you like another version of this article? Also, should I create social media posts for platforms like Facebook, Instagram, LinkedIn, and TikTok? Let me know if you’d like an email written to notify your database about this article! 😊

You said:

Please write an FAQ and a YouTube title and description

ChatGPT said:

FAQ: Home Title Theft – What You Need to Know

1. What is home title theft?

Home title theft occurs when fraudsters use stolen personal information to forge documents and transfer the ownership of your home to themselves. They can then take out loans, access equity, or even attempt to sell the property without your knowledge.

2. How common is home title theft?

While it is still relatively rare compared to other types of fraud, the rise in data breaches and online scams has made it more of a concern. Awareness and proactive protection are key to avoiding it.

3. How do scammers steal a home title?

Scammers typically:

Obtain your personal information through phishing, data breaches, or stolen mail

Forge property transfer documents

Fake a notary’s signature or bribe a notary

File fraudulent documents with the county recorder’s office

4. How can I tell if I’m a victim of home title theft?

Warning signs include:

Receiving loan statements or credit notices for accounts you didn’t open

No longer receiving mail at your home

Notifications from the county clerk about a change in ownership

Suspicious letters or calls regarding your home

5. How can I protect myself from home title theft?

You can reduce your risk by:

Freezing your credit to prevent unauthorized loans

Getting homeowner’s title insurance to protect against fraudulent claims

Regularly checking your credit report for suspicious activity

Monitoring property records for unauthorized title changes

Securing your mail to prevent identity theft

6. What should I do if I suspect home title fraud?

If you believe you are a victim of home title theft:

Contact your county recorder’s office to dispute the fraudulent title change.

Freeze your credit with Experian, TransUnion, and Equifax.

Hire a real estate attorney to help restore ownership of your property.

Alert your mortgage lender to prevent unauthorized transactions.

7. Does homeowner’s insurance cover home title theft?

No, standard homeowner’s insurance does not cover title fraud. However, homeowner’s title insurance provides protection in case of fraudulent claims on your property’s ownership.

8. Can someone really sell my house without me knowing?

It is rare, but possible. If a scammer forges documents and manages to deceive an unsuspecting buyer, they could attempt to sell your home. However, if the buyer has title insurance, they will be protected, and legal action will be taken to correct the fraud.

9. Is home title monitoring necessary?

While not essential for everyone, title monitoring services can notify you of unauthorized title changes. If you have significant home equity or concerns about identity theft, these services may provide added peace of mind.

Are you a real estate investor looking to secure financing without the hassle of traditional income verification? 🏡 DSCR loans might be the perfect solution! These loans focus on a property’s income potential rather than personal earnings, making it easier for investors to qualify and grow their portfolios.

This guide will walk you through the concept of DSCR, show you how to calculate it, and highlight its important role in real estate.

🔑Key Takeaways

The Debt Service Coverage Ratio (DSCR) is crucial for assessing the ability of a property to meet its debt obligations, as it compares net operating income to total debt service.

A DSCR of at least 1.25 is generally considered ideal for real estate investments, indicating sufficient income to cover debts and a margin for unexpected expenses.

DSCR can fluctuate 📉📈 over time due to changes in net operating income and debt service payments, making it essential for investors to monitor these variables to maintain financial health.

📊Understanding Debt Service Coverage Ratio (DSCR)

The Debt Service Coverage Ratio (DSCR) is an important tool for understanding the credit risk and debt capacity of a commercial property. At its heart, DSCR looks at how a firm’s operating income measures up against its annual debt payments and other debt obligations, giving us a quick glimpse into the financial health of the property. This ratio plays a vital role in commercial real estate, where knowing whether a property can manage its debt is crucial for making smart investment choices.

Lenders depend on DSCR to figure out the highest loan amount for new financing or refinancing options. By comparing the net operating income (NOI) to total debt service, lenders can effectively gauge a borrower’s ability to meet their debt commitments. A higher DSCR suggests a stronger financial standing, which can lead to more favorable loan arrangements and lower interest rates. On the flip side, a lower DSCR might indicate financial challenges, prompting caution for both investors and lenders.

Investors keep a close eye on DSCR as it helps them decide when to refinance and manage their risks wisely. This ratio is essential during loan discussions, assisting banks and financial institutions in minimizing lending risks. By understanding and utilizing DSCR, both investors and lenders can confidently navigate the complexities of real estate financing together.

🧮How to Calculate DSCR

Calculating DSCR is simple! Just use this formula:

📌 DSCR = Net Operating Income (NOI) ÷ Total Debt Service

To get started, you’ll need two key numbers:

1️⃣ Net Operating Income (NOI) = Total revenue minus operating expenses (excluding taxes and interest). When calculating NOI, it’s important to exclude capital expenditures to ensure an accurate representation of the property’s income potential. 2️⃣ Total Debt Service = The total amount needed to cover principal and interest payments. Total debt service includes all current debt responsibilities, such as principal and interest payments on a mortgage loan.

For example, if a property has an NOI of $500,000 and a debt service of $400,000, the DSCR would be 1.25—indicating a healthy financial position. ✅

This formula gives us a nice glimpse into how well a property generates enough income to take care of its debt payments. To get started, you’ll need two main inputs: the annual net operating income and the total annual debt service.

The first step in getting an accurate DSCR is to figure out the Net Operating Income (NOI). To calculate the NOI, just subtract certain operating expenses from the total revenue, leaving out taxes and interest. Making sure the NOI is calculated right ensures that we have a true picture of the property’s income, which is crucial for an accurate DSCR.

When we talk about total debt service, we’re looking at all current debt responsibilities. This includes not just principal and interest payments, but also sinking fund contributions and lease payments that come due within the year. There are a few factors that can affect the annual debt service, like the type of loan, interest rate, and the duration of the debt.

By keeping these factors in mind, we can ensure our DSCR calculation is spot on. Knowing how these pieces fit together helps investors assess a property’s financial health more effectively, allowing for informed decisions based on the resulting DSCR values.

Top Mortgage Lender for DSCR Loans – The Mortgage Architects

🏡 The Mortgage Architects stands out as a top mortgage broker specializing in DSCR loans, helping real estate investors secure financing without traditional income verification. With deep expertise in Debt Service Coverage Ratio (DSCR) loans, providing tailored guidance to investors looking to expand their portfolios with flexible financing solutions.

The Mortgage Architects is committed to delivering a seamless mortgage experience for investors, whether they’re purchasing rental properties, refinancing, or scaling their real estate businesses. With personalized support, experienced loan officers, and investor-friendly loan options, they help borrowers navigate the DSCR loan process and secure the best financing for their investment goals.

Significance of Net Operating Income (NOI) in DSCR

Net Operating Income (NOI) plays an important role in calculating the Debt Service Coverage Ratio (DSCR), acting as a key element in this financial evaluation. To arrive at the NOI, you simply subtract specific operating expenses from total revenue, keeping in mind that taxes and interest aren’t included in this calculation. This number becomes the foundation for evaluating a property’s capability to meet its debt responsibilities. It’s equally important to see how this links to gross operating income.

When calculating NOI, we account for expenses like maintenance and utilities while excluding taxes and interest payments. Additionally, we consider vacancy losses, which can affect the overall income that’s available to cover debts. By managing these operating expenses well, you can significantly boost your NOI, which in turn can enhance the DSCR.

A higher NOI generally signals a stronger ability to fulfill debt service requirements, providing peace of mind to lenders regarding the property’s financial well-being. Lenders often pay close attention to NOI as a way to assess the cash flow stability of a property, making it a vital piece of information in loan discussions. Therefore, grasping and effectively managing your NOI is crucial for keeping the DSCR healthy and obtaining favorable loan conditions.

4o

Ideal DSCR Values for Real Estate Investments

When it comes to real estate investments, aiming for the right DSCR values is key to financial stability. A Debt Service Coverage Ratio (DSCR) of at least 1.25 is considered a solid benchmark, showing that there’s enough net cash flow to comfortably cover debt payments and even set aside some for unexpected expenses.

It’s also important to note that different types of properties have unique ideal DSCR values.

🏢 Commercial Properties – Minimum 1.25 (higher financial risk) 🏭 Industrial Properties – 1.3 or higher (due to operational costs) 🏨 Hotels & Specialty Properties – 1.4 or above (due to unpredictable income)

For example, commercial properties typically need a minimum DSCR of 1.25 because of the higher financial risks involved. Industrial properties are often aiming for a DSCR of 1.3 or above, as they tend to have higher operational costs. Specialty properties, like hotels, usually seek a DSCR of 1.4 or more to help cushion against their unpredictable income streams.

Lenders generally look for a minimum DSCR of 1.25x when it comes to financing, which helps ensure that borrowers can manage their debts effectively.

A DSCR below 1.0 🚩 means the property isn’t generating enough income to cover its debts—something investors want to avoid! Therefore, keeping the DSCR above these suggested levels is essential for enticing investors and obtaining favorable loan conditions.

🏠Using DSCR to Evaluate Rental Properties

The Debt Service Coverage Ratio (DSCR) is an important metric for anyone looking at rental properties! It gives real estate investors a clear picture of whether a property brings in enough income to cover its mortgage payments. When the DSCR is higher, it signals better cash flow from the property, which is fantastic when you’re seeking financing.

Investors can adjust their offers based on their desired DSCR outcomes, helping them make smart property purchases that make financial sense. However, it can be tricky for investors to secure financing on properties that aren’t currently generating rental income, making a high DSCR even more crucial for getting those loans and managing risks effectively.

Plus, investors have the opportunity to pursue multiple DSCR loans at once, unlike traditional mortgages that usually limit how many properties you can have. This flexibility really empowers investors to grow their portfolios without the usual income verification hurdles, allowing them to tap into the property’s income potential for financing. Overall, the DSCR is a powerful tool for evaluating and managing rental properties!

🔄Factors Influencing DSCR Over Time

DSCR isn’t a fixed number—it changes over time based on:

📈 Increasing NOI (stronger DSCR, better refinancing options) 📉 Rising vacancy rates or expenses (lower DSCR, potential financial challenges)

Lenders have different DSCR requirements depending on property type, market conditions, and economic trends. Keeping track of these shifts helps investors maintain financial health and secure better loan terms. 💼

The Debt Service Coverage Ratio (DSCR) is a dynamic metric that can change over time due to a variety of factors. Yearly variations in DSCR can occur as a result of shifts in net operating income and fixed debt service payments. Influences like tenant turnover and the overall performance of the property play a significant role in these fluctuations.

When there’s an increase in the net income available to cover the debt, it reflects a stronger DSCR, potentially opening up more refinancing opportunities. On the other hand, if net operating income declines due to higher vacancy rates or increased maintenance costs, the DSCR may take a hit, which could suggest some financial challenges ahead.

Lenders have different minimum DSCR requirements, depending on their risk appetite, the type of property, market conditions, and the overall economic outlook. It’s important to grasp these factors and how they influence the DSCR over time to maintain a strong financial footing and secure favorable loan terms. By paying close attention to and managing these variables, investors can navigate the intricacies of real estate financing with greater confidence and ease.

🏗️DSCR in Commercial Real Estate

DSCR loans are game-changers for commercial real estate investors. Instead of verifying personal income, these loans qualify borrowers based on rental property cash flow—a huge advantage!

Why investors love DSCR loans:

✅ No income verification ✅ Ability to finance multiple properties at once ✅ Option to borrow through LLCs for asset protection

Lenders evaluate whether net operating income comfortably exceeds debt obligations, ensuring a safety net for financial fluctuations. 🏦 This way, they ensure that the property’s net operating income comfortably exceeds its debt service obligations, giving a nice safety net for any ups and downs in finances. Many investors love DSCR loans because they can borrow through LLCs, which helps keep their personal assets safe.

Additionally, DSCR loans offer amazing flexibility by allowing funding for several properties at once without needing to sell off existing ones. This feature makes them especially appealing for investors eager to grow their portfolios without being held back by traditional financing methods. So, getting comfortable with DSCR is key to successfully navigating the commercial real estate market!

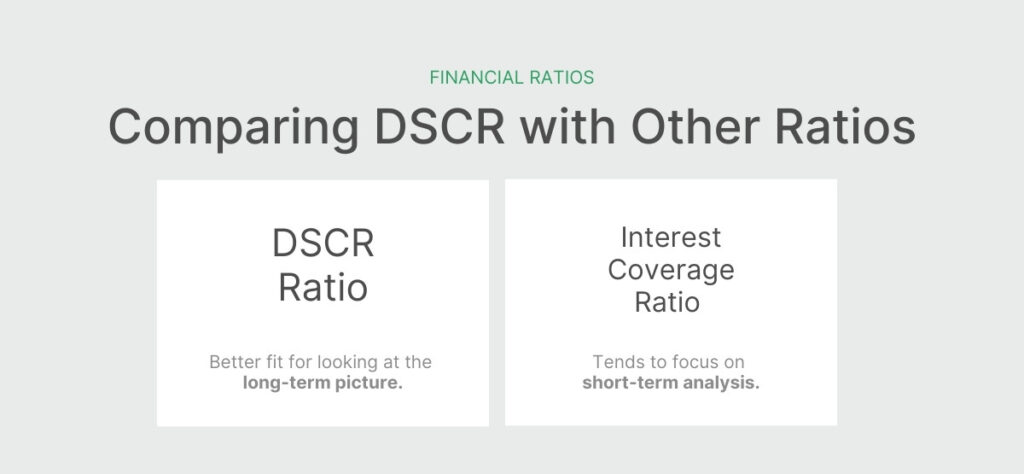

⚖️Comparing DSCR with Other Financial Ratios

When considering a company’s financial health, the Debt Service Coverage Ratio (DSCR) offers a useful comparison with other important financial ratios. For instance, the interest coverage ratio just looks at how well a company can handle its interest payments, while DSCR takes a broader view, checking if the firm can manage both interest and principal payments. This gives DSCR a fuller picture of a company’s debt responsibilities.

Although both ratios assess a company’s ability to manage debt, the interest coverage ratio tends to focus on short-term analysis, while DSCR is better for looking at the long-term picture. Generally, a higher DSCR value signals a lower risk of default for lenders, making it a vital metric in loan negotiations and investment choices.

By understanding the differences and how these ratios complement each other, investors and lenders can make smarter decisions. Using DSCR alongside other key performance indicators can help reduce risks and support financial stability in investments.

✅ Pros & Cons of DSCR

The Debt Service Coverage Ratio (DSCR) presents a mix of benefits and challenges that are important for investors to keep in mind.

Pros

One of the key benefits of having a higher DSCR is that it enhances the likelihood of obtaining better loan terms from lenders. With DSCR loans, the focus is more on the property’s cash flow instead of the borrower’s personal income, which opens up exciting possibilities for investors.

Cons

On the flip side, there are a few drawbacks to be aware of.

These loans often require a higher down payment, typically around 20% or more, which might be a hurdle for some investors.

Additionally, DSCR loans generally come with higher interest rates compared to conventional loans, which could affect long-term repayment expenses.

Plus, there’s the potential for income to be overstated since some expenses may not be included in the DSCR calculation.

It’s essential to weigh both the benefits and challenges of DSCR carefully to foster informed investment strategies. By grasping these elements, investors can feel more confident in navigating loan negotiations and making solid real estate investment choices.

Practical Examples of DSCR Calculations

Grasping the concept of DSCR becomes much clearer with practical examples! Let’s take a look at a residential rental property where the DSCR calculated was 1.4. This means there’s a lovely 40% income surplus over the debt obligations, indicating a strong financial position that would catch lenders’ eyes!

In contrast, a commercial office space example produced a DSCR of 1.06, suggesting it just manages to meet its debt obligations. This signals the potential risk of financial distress, so careful management is essential. For a multifamily property, we see a DSCR of 1.125, indicating a narrow margin of income over debt obligations.

Lastly, in a retail center scenario, the DSCR was 0.875, highlighting that the income isn’t quite enough to cover the debt payments. These real-world examples offer invaluable insights into the financial health and risk profiles of various property types, empowering investors to make well-informed decisions based on DSCR values.

Summary

Let’s summarize the key points: the Debt Service Coverage Ratio (DSCR) is a vital metric for anyone involved in real estate investments! It measures how well a property can generate the income needed to cover its debt obligations, giving valuable insights for both investors and lenders. Knowing how to calculate DSCR, manage Net Operating Income (NOI), and identify the ideal DSCR values for various property types is crucial for making smart investment choices.

In wrapping up, truly mastering DSCR can take your real estate investment strategy to the next level. By making the most of this metric, you’ll find it easier to handle loan negotiations, evaluate property performance, and reduce risks effectively. Embrace the strength of DSCR and watch your real estate endeavors reach new heights.

Frequently Asked Questions

What is the formula for calculating the DSCR ratio?

The formula for calculating the Debt Service Coverage Ratio (DSCR) is straightforward: DSCR = Net Operating Income ÷ Total Debt Service 📊 A DSCR greater than 1 means that the entity can comfortably cover its debt obligations.

How do you calculate the DSCR?

To calculate the Debt-Service Coverage Ratio (DSCR), simply divide the company’s annual net operating income (NOI) by its total annual debt service, which includes both principal and interest payments. For example, if a property boasts an NOI of $500,000 and has a debt service of $400,000, the DSCR would come to 1.25.

What is a good DSCR ratio?

Generally, a good Debt Service Coverage Ratio (DSCR) is considered to be above 1.25, while a ratio of 2.0 or higher is seen as exceptionally strong. Ratios below 1.00 can hint at possible financial difficulties.

What is the Debt Service Coverage Ratio (DSCR)?

The Debt Service Coverage Ratio (DSCR) is a financial measure that evaluates a property’s ability to generate enough income to meet its debt obligations, calculated by dividing net operating income (NOI) by total debt service. A DSCR greater than 1 indicates that income surpasses debt obligations, pointing to financial stability.

Why is a DSCR of 1.25 considered good?

A DSCR of 1.25 is regarded as good because it shows that the property earns 25% more than necessary to cover its debt, providing a nice cushion for unexpected expenses and enhancing overall financial security.

Should I lock it or not? Many homebuyers are stuck in “analysis paralysis,” debating whether to lock their rate or wait for potential improvements. However, delaying your rate lock can cost you thousands of dollars.

In this guide, we’ll break down: ✅ Why locking your rate is crucial ✅ The risks of waiting ✅ How lenders price mortgage rates ✅ Ways to mitigate losses if rates improve

Let’s dive in!

What is a Mortgage Rate Lock?

A mortgage rate lock is an agreement between you and your lender that ensures your interest rate won’t change for a specified period—typically 30, 45, or 60 days.

Why does this matter? Because mortgage rates fluctuate daily based on economic factors, market conditions, and Federal Reserve policies. Locking your rate safeguards you from unexpected increases.

The Risks of Not Locking Your Rate

1. Market Volatility Can Cost You Thousands

Mortgage-backed securities (MBS) determine interest rates, and they behave like the stock market—constantly moving.

Green means good (rates drop, loans become cheaper).

Red means bad (rates increase, making your mortgage more expensive).

Some days, rates fluctuate dramatically. If you delay locking in your rate and the market shifts overnight, your mortgage payment could become significantly more expensive.

💡 Example: Let’s say you’re financing a $500,000 home with an interest rate of 6.5% at no additional cost. If the market worsens the next day and that same rate now costs $2,500 upfront, you’ve just lost out by waiting.

2. Waiting for Lower Rates is a Gamble

Some buyers try to “time the market,” hoping rates will drop before they lock in. The problem? The mortgage market is unpredictable.

Lenders hedge their risk by pricing rates conservatively.

Even if rates drop slightly, lenders won’t pass all those savings on to you.

A worsening market can drive rates up significantly in just one day.

🏠 Key takeaway:It’s better to lock in a solid rate now than risk a sudden increase.

Why Lenders Always Win in Rate Pricing

Mortgage lenders operate like a casino—the odds favor them. Here’s how:

1. Downward Market = Higher Costs for You

If rates rise, lenders increase pricing quickly to protect their profits. You, the borrower, bear the cost.

2. Upward Market = Minimal Savings Passed to You

If rates drop, lenders adjust pricing slowly, ensuring they still benefit.

📊 Bottom line:Lenders position themselves to minimize their risk. You should too—by locking in your rate.

How to Mitigate the Risk of a Rate Drop After Locking

Some buyers worry about locking too early—what if rates improve? Here’s the good news:

✔️ Switching Lenders – If a better rate becomes available, an independent mortgage broker (like us!) can move your loan to another lender with better pricing.

✔️ Rate Renegotiation – Some lenders allow a one-time “float down” option to lower your rate if the market shifts favorably.

✔️ Loan Pricing Adjustments – Once locked, you can still adjust the loan structure (paying points for a lower rate or taking lender credits for closing cost savings).

Loan Amount & Rate Changes: How Much Does It Matter?

The bigger your loan, the greater the impact of interest rate fluctuations.

🔢 Example Calculation:

Loan Amount: $500,000

Interest Rate: 6.5%

Cost for that rate: 0.5 points (0.5% of the loan)

Total Cost: $500,000 × 0.005 = $2,500

💰 A 1% rate increase on a $700,000 loan could cost you over $7,000 upfront or hundreds per month.

The Overnight Rate Change Scenario

📅 Day 1: You’re under contract, and your lender provides rate options.

🔄 Day 2: You decide to wait… but the market shifts.

🚨 Result:

That 6.5% rate is no longer free—it now costs $2,500+ upfront.

Your payment increases, or you pay thousands extra at closing.

😟 Avoid this mistake—lock your rate when given the opportunity!

Key Takeaways: How to Make the Right Decision

✅ Lock your rate early – Market volatility can cost you significantly overnight. ✅ Don’t wait for a perfect rate – Trying to time the market is risky. ✅ Lenders always hedge their risk – Protect yourself by securing a rate. ✅ Loan size matters – The larger your loan, the bigger the impact of changes. ✅ You can still switch lenders – An independent mortgage broker can help you find the best rate after locking.

📣 Ready to secure your rate and protect your finances? Contact us today for expert guidance!

Would you like a shorter version of this article or a social media post for platforms like Instagram, LinkedIn, and TikTok? Let me know, and I’ll tailor the content for different audiences! 🚀

You said:

Can you write an FAQ for this article?

ChatGPT said:

FAQ: Mortgage Rate Locks – Everything You Need to Know

1. What is a mortgage rate lock?

A mortgage rate lock is an agreement between you and your lender that secures a specific interest rate for a set period (usually 30, 45, or 60 days). This ensures that your rate won’t change due to market fluctuations while your loan is being processed.

2. Why should I lock my mortgage rate?

Locking your rate protects you from unexpected interest rate increases. Mortgage rates fluctuate daily based on economic news, inflation, and market conditions. If you don’t lock, your rate could go up overnight, costing you thousands more over the life of your loan.

3. When should I lock my mortgage rate?

You should lock your mortgage rate as soon as you are comfortable with the rate being offered and are under contract for a home. The longer you wait, the more you risk market volatility increasing your rate.

4. What happens if I don’t lock my rate?

If you don’t lock your rate and the market shifts, your mortgage could become significantly more expensive. A rate increase of just 0.5% could cost you thousands in upfront fees or increase your monthly payment by hundreds of dollars.

5. Can I wait for rates to improve before locking?

You can, but it’s risky. Mortgage markets are unpredictable, and lenders adjust rates quickly to protect themselves. If rates do drop, lenders may not pass all the savings to you. If rates go up, you’ll be stuck paying more.

6. What if I lock my rate and then rates go down?

If rates drop significantly after you lock, you may have options:

Rate renegotiation (float-down option): Some lenders allow a one-time adjustment if market conditions improve.

Switching lenders: If a different lender offers a better rate, an independent mortgage broker can move your loan.

Loan structure changes: You may be able to adjust your loan terms to take advantage of lower rates.

7. How do lenders decide mortgage interest rates?

Mortgage rates are based on the movement of mortgage-backed securities (MBS) in the financial markets. When MBS prices rise, rates decrease, and when MBS prices drop, rates increase. Other factors influencing rates include inflation, Federal Reserve policies, and global economic conditions.

8. What does it mean when people say ‘floating’ a mortgage rate?

Floating means choosing not to lock your rate and waiting to see if the market improves. This is risky because if rates increase, you’ll be stuck paying more. Locking eliminates this uncertainty.

9. Does locking my rate cost anything?

Rate locks typically do not have a direct cost unless you choose a longer lock period (e.g., 90 days). However, delaying a lock and seeing rates increase can result in higher costs in the form of higher interest rates or upfront fees (points).

10. What is ‘par pricing,’ and why does it matter?

Par pricing means you’re getting a rate with no extra cost to you. If a lender quotes you a 6.5% interest rate at par pricing, it means you aren’t paying extra fees (points) to get that rate. However, if the market worsens overnight, the same rate may now cost thousands upfront.

11. What are mortgage points, and how do they affect my loan?

Mortgage points (discount points) are fees paid upfront to lower your interest rate. One point equals 1% of your loan amount. For example, on a $500,000 loan:

0.5 points = $2,500 upfront

1 point = $5,000 upfront

If the market shifts overnight, you may have to pay more points to keep the same rate.

12. What if I lock my rate but my closing is delayed?

If your closing takes longer than your rate lock period, you may need a rate lock extension. Some lenders charge for this, while others offer a free extension under certain conditions.

13. Can I change my mortgage rate after locking?

Yes, but with limitations. Once locked, your entire rate sheet is locked. You can still adjust within those options (choosing a slightly higher or lower rate with different pricing), but you can’t access new rates that came after your lock date.

14. Does my loan amount affect how much rates impact me?

Yes! The larger your loan, the bigger the financial impact of rate changes. For example, a 0.5% increase on a $700,000 loan is far more costly than the same increase on a $200,000 loan.

15. What if I lock my rate and then change lenders?

If you work with an independent mortgage broker, they can move your loan to a different lender if a better rate becomes available. This is a major advantage of working with a broker versus a bank.

16. Is there ever a reason NOT to lock my mortgage rate?

Very rarely. The only time you might hold off on locking is if you have strong insider knowledge that rates will drop significantly in the short term and you can afford to take the risk. For most buyers, locking as soon as possible is the best choice.

17. Can I lock my rate before I find a home?

Some lenders offer “lock and shop” programs that let you secure a rate before you have a property under contract. This can be useful in rising rate environments.

18. What’s the difference between a broker and a bank when locking rates?

Banks only offer their own loan products, so you’re stuck with their rates.

Brokers have access to multiple lenders (sometimes 50+), giving you flexibility to switch if rates improve elsewhere.

19. Can I break my rate lock if I change my mind?

Generally, no. Once you lock, you’re committed unless you switch lenders or pay a penalty (if applicable). However, a broker can help you explore alternative lenders if needed.

20. What’s the biggest mistake homebuyers make with rate locks?

The biggest mistake is waiting too long and missing a good rate. Rates can change overnight, and once they increase, there’s no way to go back. Locking early protects you from unnecessary financial risk.

Final Takeaway:Locking your mortgage rate early is the best way to protect yourself from market uncertainty. If you have more questions or need expert guidance, reach out today!

Buy vs. Wait? When considering buying a home, the timing often feels tied to interest rates. Many potential buyers take a step back from the market, hoping to wait out high rates. The idea is simple: wait for rates to drop, and the home purchase will become more affordable.

While this sounds logical, the reality is far more complex—and waiting might end up costing you far more in the long run. Let’s break down why buying now could actually save you money compared to waiting for a hypothetical drop in interest rates.

The Current Market: A Buyer’s Advantage

At first glance, buying in a market with high interest rates and elevated home prices seems unwise. However, fewer buyers in the market create significant opportunities for savvy homebuyers. Here’s why:

1. Less Competition

When interest rates rise, many buyers put their plans on hold. This reduces competition in the market, giving active buyers an advantage. Sellers often find their homes sitting on the market longer, leading them to reduce prices or offer incentives to close the deal.

More negotiating power: Sellers are more willing to entertain offers below the list price.

Seller concessions: Sellers may offer to cover closing costs or other fees, reducing your out-of-pocket expenses.

2. Price Reductions

In a competitive market, homes often sell at or above the asking price. When the market cools, sellers may need to lower their prices to attract buyers, creating opportunities to purchase a home at a discount.

The Waiting Game: A Costly Gamble

Many buyers delay their purchase hoping for lower interest rates. While this may seem like a smart move, it can cost more in the long run due to:

1. Rising Home Prices

Home values historically appreciate over time. Even in slower markets, national averages show a 4-5% annual increase in home prices. Waiting a year or more could mean paying significantly more for the same home.

Example: A $350,000 home today could appreciate to $375,000 or more within a year, adding $25,000 to the purchase price.

2. Missed Equity

By purchasing now, you start building equity immediately. Renting during the waiting period means you’re paying someone else’s mortgage rather than investing in your own property. Even with higher interest rates, owning allows you to capture future appreciation and build wealth.

3. Market Crowding

When rates drop, buyers flood the market. Increased demand drives up home prices and reduces negotiating power. In a bidding war, you’re less likely to secure seller concessions or a discounted price.

The Numbers: Buying Now vs. Waiting

Let’s examine a real-world example comparing the cost of buying now versus waiting a year for rates to drop.

In this scenario, you purchase the home at a lower price, negotiate concessions, and begin building equity immediately.

Scenario 2: Waiting One Year

Home Price: $375,000 (with 5% appreciation)

Interest Rate: 5.5%

Down Payment (5%): $18,750

Monthly Payment (Principal & Interest): $2,851

While the monthly payment is slightly lower, the increased home price means you bring more cash to closing and lose out on $25,000 in equity from appreciation. Additionally, you’re less likely to secure seller concessions in a competitive market with lower rates.

Key Takeaways:

Equity Loss: By waiting, you lose out on $25,000 in appreciation that would have been yours had you purchased earlier.

Minimal Savings: The $72 monthly savings in the lower interest rate doesn’t outweigh the higher purchase price.

Lost Opportunity: If you’ve been renting, you’ve spent money on rent rather than investing in your future.

Refinancing: The Game Changer

One of the biggest misconceptions is that a high interest rate locks you in forever. The truth is, refinancing offers an opportunity to reduce your rate later. Here’s how refinancing works to your advantage:

Refinance at Lower Rates: When rates drop, you can refinance to secure a lower monthly payment.

Build Equity Faster: By purchasing now, you’ve already started building equity, meaning your refinance is based on a smaller loan balance.

Lower Long-Term Costs: A refinance at a lower rate later can save you significantly, especially compared to the higher costs of waiting to buy.

Example: Refinancing After 1 Year

Loan Amount (after 1 year): $336,000 (down from $350,000 due to equity build-up)

Refinanced Interest Rate: 5.25%

New Monthly Payment: $2,633 (saving $289/month compared to the original payment)

Even with a refinance, purchasing now allows you to lock in a lower purchase price and start saving sooner.

Why Time in the Market Matters More Than Timing the Market

The old adage applies: “It’s not about timing the market; it’s about time in the market.” Buying sooner allows you to:

Start building equity immediately.

Take advantage of current market conditions with fewer buyers.

Avoid higher home prices caused by appreciation.

While waiting may seem like a safer option, the numbers show that acting now provides more financial benefits over time.

Key Benefits of Buying Now

Negotiation Power: Fewer buyers mean more room to negotiate on price and concessions.

Lower Competition: Avoid bidding wars and pay less over the list price.

Equity Growth: Start building wealth immediately, even at higher rates.

Refinance Opportunities: Lower your rate in the future without losing out on today’s deals.

Final Thoughts

While interest rates can feel like the biggest factor in deciding when to buy, they’re only one piece of the puzzle. Appreciation, competition, and seller concessions play equally important roles in determining the overall cost of homeownership. By buying now, you can take advantage of a quieter market, start building equity, and set yourself up for long-term financial success.