What Is a Mortgage Discount Point? Exploring the Basics and Benefits

Buying a home is a significant financial decision, and understanding the intricacies of mortgages can feel overwhelming. One aspect you might encounter is “what is a mortgage discount point”, which can impact your interest rate and monthly payments. This article will shed light on the concept of mortgage discount points, their cost, and whether they are the right choice for you. Let’s dive in!

Key Takeaways (aka: The Cliff Notes)

- Mortgage discount points can lower interest rates, but it’s important to consider the pros and cons before investing.

- Calculate the breakeven point to determine if buying mortgage points is worth it for your individual financial situation.

- Using a mortgage broker like The Mortgage Architects means your broker will do the research, shop many loan providers, and negotiate better terms on your behalf.

Understanding Mortgage Discount Points

Mortgage discount points are fees paid upfront to lower the mortgage interest rate on your home loan. Buying mortgage points can be a sound investment if you plan to stay in your current home for an extended period. To better understand how mortgage points work, consider that staying in your home for over 10 to 15 years or even longer can make this investment worthwhile.

However, there’s a downside: you’ll have to pay more in closing costs to enjoy a lower monthly payment for the life of the loan. So, it’s essential to weigh the benefits and drawbacks of paying points.

The Difference Between Discount Points and Origination Points

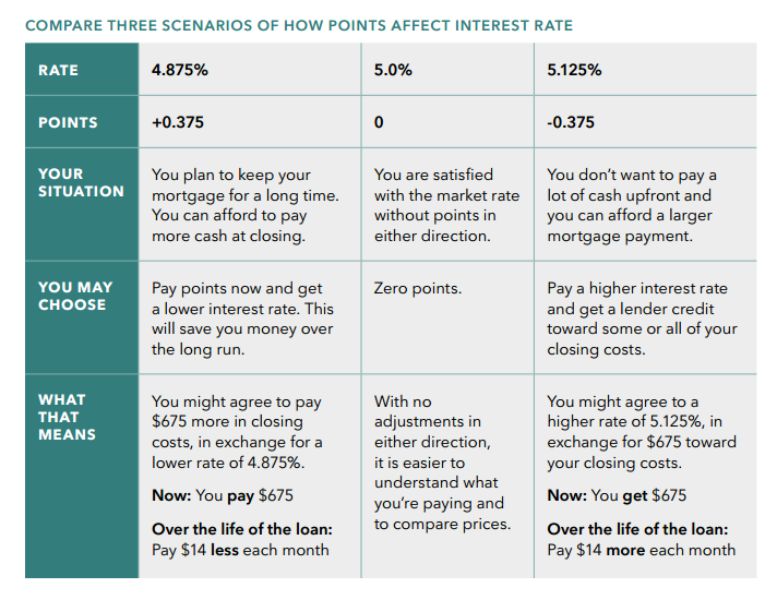

While both discount points and origination points are fees associated with mortgages, they serve different purposes. Discount points lower the interest rate on your mortgage loan, while origination points are mandatory fees charged by lenders for processing the loan. Each discount point costs 1% of the loan amount and usually reduces the rate by 0.25%.

It’s possible to negotiate a better deal on discount points and origination points, especially if you have a 20% down payment, a good credit score, and you’re a well-qualified buyer. Some lenders might offer no origination points but with higher interest rates. Keep in mind that mortgage points may have tax-deductible benefits.

Cost of Mortgage Discount Points

Mortgage discount points typically cost 1% of the loan amount per point and are included in the closing costs. To put this into perspective, if you buy a half-point on a $300,000 mortgage, it would cost $1,500.

It’s crucial to weigh the long-term benefits of purchasing discount points against the upfront cost. By calculating the difference between the cost of the points and the interest you’ll save over the life of the loan, you can determine if buying mortgage points is a financially sound decision.

How Mortgage Discount Points Work

Mortgage discount points, also known as points on a mortgage, are fees you pay at closing to secure a lower interest rate on your home loan. The number of points you can buy depends on the type of mortgage loan and the general interest rate climate, with most lenders allowing up to four points. You can even buy parts of a mortgage discount point.

When purchasing discount points, it’s essential to consider the breakeven period – the time it takes for the monthly savings from the lower interest rate to equal the upfront costs of the discount points. This period can help you determine if paying points is a wise financial decision.

For example, if you plan to stay in your home longer than the breakeven point without refinancing, it might be worth it to pay points. If you keep the loan beyond the breakeven point, the interest rate reduction will continue to provide monthly savings for the life of the loan.

Mortgage Discount Points Example

To better understand the potential benefits of mortgage discount points, let’s consider an example. A borrower buys two discount points for $6,400 upfront, which lowers their interest rate to 6.5%. Over the life of the loan, they save a substantial $38,286 in interest.

To calculate the breakeven point, divide the cost of the mortgage points ($6,400) by the monthly savings from the reduced interest rate. This calculation will help you determine if buying points is financially beneficial, given your plans for the property and the length of time you intend to hold the loan with monthly mortgage payments.

Determining the Value of Mortgage Discount Points

The value of mortgage discount points depends on factors such as how long you plan to stay in the home and the amount of money available for upfront costs. To determine if buying points is worth it, calculate the breakeven point and compare it to your expected length of stay in the property.

This will help you decide if it is worth it to buy points or not. Consider the amount of money.

Calculating the Breakeven Point

The breakeven point is the amount of time it takes for the monthly savings from the lower interest rate to equal the upfront costs of the discount points. This calculation involves dividing the cost of mortgage points by the monthly savings from the lower interest rate. Factors that affect the breakeven point include the loan size, interest rate, and discount points.

By comparing the breakeven point to your planned length of stay in the property, you can determine if purchasing discount points is a good financial decision. If the breakeven point is shorter than your expected length of stay, buying points could be a wise choice.

Pros and Cons of Mortgage Discount Points

There are advantages and disadvantages to consider when deciding whether to buy mortgage discount points. On the plus side, discount points can lead to potential long-term savings, lower monthly payments, and tax deductions. However, you must also take into account the increased upfront costs and the need to stay in the home long enough to recoup the investment.

Ultimately, the decision to purchase mortgage discount points depends on your individual financial situation and goals. It’s essential to weigh the pros and cons, calculate your breakeven point, and consider the length of time you plan to stay in your home before making a decision.

Mortgage Discount Points and Taxes

Mortgage discount points are tax-deductible as prepaid interest, which can provide additional financial benefits for borrowers. However, there are limitations on the amount that can be deducted. Deductions are allowed on the first $750,000 borrowed. For example, if you have a $1 million mortgage and purchase one point for $100,000, only $75,000 (1% of $750,000) can be deducted.

It’s advisable to consult a tax professional to determine how much of the mortgage discount points can be deducted from your taxes. They can help you navigate the tax implications and ensure you’re taking full advantage of any available deductions.

Comparing Mortgage Loan Offers with Discount Points

When comparing mortgage loan offers, it’s important to consider the Annual Percentage Rate (APR), which includes the effects of discount points, as well as loan terms and closing costs. The APR accounts for not just the interest rate, but also the points you pay and any fees the lender charges, making it easier to compare loans.

Before accepting a quote from a lender, be sure to analyze the numbers and determine if paying points to get a lower rate is the best option for your financial situation. Use a mortgage broker who will shop around on your behalf to find the best deal and secure lower interest rates.

Tips for Negotiating Mortgage Discount Points

Negotiating mortgage discount points is possible, but not guaranteed. To improve your chances, use a mortgage broker to shop around and apply to multiple lenders (with one application) to find the best deal and potentially secure lower interest rates. Keep in mind that your options may depend on factors such as your credit score, down payment, and overall financial situation.

It’s also helpful to work with a loan officer who can explain your Loan Estimate or truth-in-lending disclosure, ensuring you fully understand the terms and costs associated with your mortgage. By being well-informed and proactive in your search for mortgage lenders, you can increase your chances of securing the best mortgage deal for your needs.

Summary

Mortgage discount points can be a valuable tool for homebuyers, allowing you to secure a lower interest rate and potentially save thousands of dollars over the life of your loan. However, it’s essential to consider the upfront costs and the length of time you plan to stay in your home before deciding to purchase points. By understanding the concept of mortgage discount points, calculating the breakeven point, comparing loan offers, and negotiating with lenders, you can make an informed decision and secure the best possible mortgage deal for your needs.

Frequently Asked Questions

How much does 1 discount point lower your rate?

On average, one discount point will lower your rate by 0.25 percent. This means that if your current mortgage rate is 5 percent, one discount point would reduce it to 4.75 percent, and two discount points would reduce it to 4.50 percent.

How much is 2 discount points on a mortgage?

Two discount points on a mortgage is equivalent to two percent of the loan amount. That means, for a loan of $100,000, you would be paying $2,000 in discount points.

This payment is typically made at closing.

What is an example of a discount point?

An example of a discount point is when you pay an upfront fee to reduce the interest rate on your loan. This fee, which is usually one percent of the total loan amount, can save you money over the life of the loan.

How do mortgage discount points affect my interest rate?

Mortgage discount points are a great way to reduce your interest rate – each point will cost 1% of the loan amount and usually decrease the rate by 0.25%. So, it’s worth considering investing in points if you want to save money on interest payments.

What is the difference between discount points and origination points?

Discount points are an optional fee that can be paid to lower your interest rate, whereas origination points are a mandatory fee that comes with taking out a loan.