Are you a non-US citizen looking to purchase a home but don’t have a Social Security Number (SSN)? ITIN mortgage loans might be the solution to your homeownership dreams. Discover fresh perspectives on ITIN loans and learn how they provide unique opportunities for non-US citizens to achieve their goals of owning a home in the United States. Download our ITIN brochure here.

Key Takeaways

- ITIN loans provide an alternative path to homeownership for non-US citizens & their dependents.

- Requirements include having a credit score in the high 600s, providing tax returns and proof of assets, and putting down a minimum 11% down payment.

- Mortgage Architects are top lenders for ITIN loans with personalized guidance & Spanish language services available.

Understanding ITIN Loans: A Comprehensive Guide

ITIN mortgage loans are a specialized type of mortgage designed for people who have an Individual Taxpayer Identification Number (ITIN) instead of an SSN. These loans cater to non-US citizens, offering unique eligibility criteria and terms for homebuyers who possess an ITIN. So, even if you don’t have a Social Security Number, you can still qualify for an ITIN loan and step into the world of homeownership.

ITIN loans are available for both residents and non-residents who aren’t US citizens, as well as their spouses. This alternative form of financial help provides a path to homeownership for those without an SSN and their dependents. The mortgage process for ITIN loans is similar to that of traditional mortgages but with some additional requirements to consider.

How ITIN Loans Work

At their core, ITIN loans function like traditional mortgages. The main difference is that they cater to borrowers with ITINs instead of SSNs. They are considered non-qualified mortgages due to not meeting the lending guidelines set by the CFPB, which can result in higher costs for borrowers since they are deemed riskier. However, the ITIN mortgage program aims to help non-US citizens and residents without a Social Security Number achieve homeownership.

The terms and conditions of ITIN loans can differ depending on the lender and their policies. Some usual conditions include needing a down payment, possessing a taxpayer ID number instead of an SSN, and other terms that might apply. Keep in mind that not everyone qualifies for an ITIN loan, and mortgage rates for ITIN loans may be higher than those for conventional loans.

Despite their unique characteristics, itin home loans have proven to be a viable home financing option for non-US citizens. They provide many borrowers with the opportunity to purchase a home in the United States, and in doing so, help them build credit and establish a stable financial future.

ITIN Program Requirements

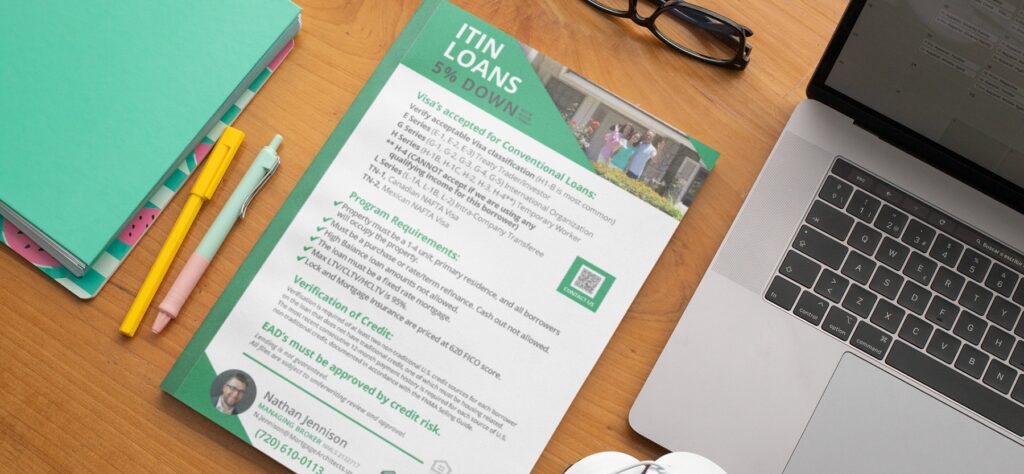

Certain program requirements must be met to qualify for an ITIN loan. The property you wish to purchase must meet the following criteria:

- It must be a 1-4 unit primary residence

- All borrowers will occupy the property

- It must be a purchase or rate/term refinance (cash out not allowed)

- High balance loan amounts and adjustable-rate mortgages are not permitted

- The maximum LTV/CLTV/HCLTV is 95%.

In terms of eligibility, you’ll need to have enough income and assets, provide tax returns, show proof of assets, have been employed consistently for two years, have a credit score in the high 600s, and put down a minimum down payment of 11%. You can use ITIN loans to buy single-family homes, townhomes, condos, and multi-family dwellings.

ITIN Loan Eligibility Requirements

Specific requirements must be kept in mind concerning ITIN loan eligibility. To be eligible for an ITIN loan, the following criteria must be met:

- Verification is required for at least two non-traditional U.S. credit sources for each borrower on the loan who doesn’t have traditional credit.

- One of these non-traditional U.S. credit sources must be housing-related.

- The most recent consecutive 12-month payment history is required for each source of U.S. non-traditional credit.

These requirements aim to ensure that borrowers have a stable and verifiable financial background before being granted an ITIN loan. By verifying non-traditional credit sources and payment history, lenders can better assess the risk associated with lending to borrowers without traditional credit scores.

Top Mortgage Lender for ITIN Loans – The Mortgage Architects

The Mortgage Architects emerge as one of the top mortgage lenders in the realm of ITIN loans. With experience in the ITIN mortgage program, they provide personal home buying guides to help borrowers navigate the process. They also have Spanish-speaking loan officers, making it easier for ITIN loan applicants who prefer to communicate in Spanish.

The Mortgage Architects is committed to providing the best possible mortgage experience for ITIN loan borrowers, including those seeking itin mortgages. By offering personalized guidance, experienced loan officers, and a user-friendly website in Spanish, they cater to the unique needs of ITIN borrowers and help them find the best mortgage lender for their situation.

Comparing Interest Rates and Terms

Comparing interest rates and terms is a vital part of searching for the best ITIN loan provider. Interest rates for ITIN loans can vary depending on the lender and the loan’s terms. Here are some key points to consider:

- Rates typically range from around 7.375% to 8.750%.

- ITIN loan interest rates might be higher than those for conventional or FHA loans.

- Borrowers with limited credit history are seen as riskier, which can contribute to higher interest rates.

However, by comparing different lenders and loan options, you can find the best mortgage option for your unique financial situation. You should consider factors such as the loan term, interest rate, and any additional fees or charges when comparing ITIN loan providers.

Another aspect to consider when looking for an ITIN loan is refinancing options. Borrowers with ITIN loans may be eligible for a rate and term refinance to lower their interest rate or change the loan term. This can help borrowers secure better loan terms and potentially save money over the life of the loan.

Essential Documentation for ITIN Loan Applications

Having all the essential documentation ready contributes to a smooth ITIN loan application process. This includes:

- Proof of income

- Employment history

- Tax returns

- Credit history

Providing accurate and complete documentation, including bank statements, can help streamline the application process and increase your chances of loan approval.

Lenders typically require at least 12 months of consistent employment and may request additional documents to verify your income and assets. Ensuring that you have all the necessary paperwork organized and ready for submission can help prevent delays or rejection of your ITIN loan application.

Tips for Streamlining the Application Process

Being organized and submitting all required documentation promptly and accurately can streamline the ITIN loan application process. This can help increase your chances of loan approval and make the process smoother overall.

Some tips for streamlining the ITIN loan application process include gathering all necessary documents, such as proof of income, employment history, and tax returns, before applying. Additionally, it’s crucial to double-check your application for any errors or missing information before submitting it to the lender. By being organized and thorough with your application, you can help ensure a smooth and successful ITIN loan approval process.

Pros and Cons of ITIN Mortgage Loans

Borrowers should consider the benefits and drawbacks of ITIN mortgage loans when deciding if this type of loan suits their needs. On the one hand, ITIN loans provide expanded homeownership opportunities for non-US citizens who might otherwise have difficulty obtaining a traditional mortgage.

On the other hand, ITIN loans can come with potentially higher interest rates, larger down payments, and limited lender options compared to traditional mortgage loans. It’s essential for borrowers to weigh the pros and cons of ITIN loans to determine if they are the best option for their unique financial situation.

Benefits of ITIN Loans

One of the main benefits of ITIN loans is that they provide access to homeownership for non-US citizens who might not be eligible for traditional home loan options. ITIN loans offer more flexible credit requirements, making it easier for borrowers with limited credit history to qualify.

In addition to providing a path to homeownership, ITIN loans can also offer potential tax advantages for borrowers. By allowing non-US citizens to purchase a home in the United States and establish a credit history, ITIN loans can help borrowers improve their overall financial standing and potentially qualify for other loans in the future.

Drawbacks of ITIN Loans

Despite their benefits, ITIN loans also come with some drawbacks. One of the main downsides is that they can have higher interest rates than traditional mortgage loans, as they are considered riskier due to the limited credit history of borrowers. This can result in higher monthly payments and overall costs for borrowers over the life of the loan.

Another drawback is that ITIN loans may require larger down payments than traditional mortgages. Additionally, lender options for ITIN loans are limited, as not all lending institutions offer these types of loans. Despite these drawbacks, ITIN loans can still be a viable option for non-US citizens looking to purchase a home in the United States.

Tips for Improving Your Chances of ITIN Loan Approval

Thorough preparation for the home buying process can improve your chances of ITIN loan approval. This includes building a solid credit history, saving for a down payment, and researching lender options that specialize in ITIN loans.

By understanding the unique requirements of ITIN loans and taking the time to gather all necessary documentation, borrowers can increase their chances of loan approval. Working with a knowledgeable lender who understands the ITIN loan process can also help guide borrowers through the application process and ensure a higher likelihood of success.

Preparing for the Home Buying Process

Understanding the specific requirements and gathering all necessary documentation are key when preparing for the home buying process with an ITIN loan. This includes:

- Proof of income

- Employment history

- Tax returns

- Credit history

Working with a knowledgeable lender who specializes in ITIN loans can help guide borrowers through the application process and ensure a higher likelihood of success.

By being proactive in gathering all required documents and understanding the unique requirements of ITIN loans, borrowers can set themselves up for a successful home buying experience. Taking the time to research lender options and work with a lender who understands the ITIN loan process can greatly improve the chances of loan approval and make the journey to homeownership a smoother one.

Refinancing Options for ITIN Loans

Borrowers looking to secure better interest rates or loan terms might find refinancing options for ITIN loans beneficial. Depending on eligibility requirements and financial goals, refinancing an ITIN loan can help lower monthly payments, get a better interest rate, or adjust the loan term.

By considering refinancing options, borrowers with ITIN loans can explore ways to improve their financial situation and potentially save money over the life of the loan. It’s essential to carefully evaluate the benefits and drawbacks of refinancing an ITIN loan to determine if it’s the right choice for your unique circumstances.

Eligibility Requirements for Refinancing

While eligibility requirements for refinancing ITIN loans may vary by lender, they typically involve considerations of credit history, income stability, and property value. Lenders will assess your capacity to pay back the loan, so providing evidence of income and employment is essential.

Property value can also affect eligibility for ITIN loan refinancing, as lenders usually have a maximum loan-to-value ratio they’ll refinance. By understanding the eligibility requirements for refinancing and working with a lender who specializes in ITIN loans, borrowers can explore the potential benefits of refinancing and make informed decisions about their financial future.

Summary

ITIN mortgage loans provide a unique opportunity for non-US citizens to achieve homeownership in the United States. With benefits like flexible credit requirements and potential tax advantages, ITIN loans can be a viable option for many borrowers. However, it’s crucial to weigh the pros and cons, such as potentially higher interest rates and limited lender options, before deciding if an ITIN loan is the right choice for you. By understanding the ITIN loan process, preparing for the home buying journey, and working with experienced lenders like The Mortgage Architects, you can take the first steps toward achieving your dream of homeownership in the United States.

Frequently Asked Questions

Can I get a loan with my ITIN number?

Yes, it is possible to get a loan with your ITIN number. Many financial institutions allow you to access personal loans, bank accounts and credit cards, giving you an opportunity to build a credit history in the US.

Who qualifies for an ITIN loan?

ITIN loans are ideal for non-resident aliens, foreign nationals and their spouses and dependents, who are not eligible for SSNs. To qualify, you’ll typically need a high credit score and a down payment of at least 11%.

What is a ITIN loan program?

ITIN loans are an available option for those without a Social Security number, enabling them to get a mortgage provided they meet certain eligibility criteria.

Can you get a Fannie Mae loan with an ITIN number?

Fannie Mae requires both a valid Social Security number and an ITIN for borrowers, so you can get a loan with an ITIN number.

What are the main benefits of ITIN loans?

ITIN loans provide non-US citizens with access to homeownership, flexible credit requirements, and potential tax advantages, making them an appealing option.

Related Resources

Gift Funds: How Parents Can Help Their Kids Buy Their First Home