A DSCR loan is designed for real estate investors who want to qualify for financing based primarily on the income an investment property is expected to produce.

DSCR stands for Debt Service Coverage Ratio. In residential investment lending, it helps answer a straightforward question:

Does the property generate enough rental income to cover its monthly housing debt?

This guide focuses on residential investment-property DSCR loans. It does not cover traditional owner-occupied mortgages or large-scale commercial lending.

A borrower using a DSCR loan must purchase or refinance the property as an investment property and certify that they will not live in it as a primary residence or second home. That occupancy requirement matters because the loan is underwritten based on the property’s rental income—not the borrower’s personal income or traditional debt-to-income ratio.

Principales conclusiones

- DSCR stands for Debt Service Coverage Ratio.

- A residential DSCR calculation generally compares the property’s qualifying monthly rent to its total monthly housing payment.

- Total debt service usually includes principal, interest, property taxes, homeowners insurance, and applicable HOA fees.

- A DSCR of 1.00 means the property’s qualifying rental income equals its monthly housing expense.

- A DSCR above 1.00 provides some cash-flow cushion. A ratio of 1.25 is a strong target, but it is not required by every lender.

- Many lenders can work with a DSCR of 1.00 or better. Some loan programs allow ratios below 1.00—or no-ratio DSCR loans—with higher interest rates, costs, or other compensating factors.

- Long-term rental income and short-term rental income are calculated differently.

- DSCR loans are for investment properties only; the borrower cannot occupy the property.

What Is Debt Service Coverage Ratio (DSCR)?

The debt service coverage ratio, or DSCR, measures whether a rental property’s income can support the monthly debt obligations tied to that property.

For a residential DSCR loan, the lender is typically not trying to qualify the borrower through W-2 income, tax returns, pay stubs, or a traditional debt-to-income calculation. Instead, the lender evaluates whether the rental property itself can support the proposed mortgage payment.

That makes DSCR financing especially useful for real estate investors, self-employed borrowers, and people building a rental-property portfolio.

A DSCR loan does not mean that the borrower’s credit, reserves, down payment, or assets are irrelevant. Lenders still review the overall loan scenario. However, the property’s rental income is the centerpiece of the DSCR calculation.

DSCR Formula: How to Calculate DSCR

For the residential investment-property DSCR loans discussed here, the formula is:

DSCR = Qualifying Monthly Rental Income ÷ Total Monthly Debt Service

The result is expressed as a ratio.

For example:

- Qualifying monthly rental income: $3,000

- Total monthly debt service: $2,500

$3,000 ÷ $2,500 = 1.20 DSCR

That means the property’s qualifying rent is 120% of its monthly housing expense.

Calculate the Debt Service

For a residential DSCR loan, total debt service generally means the full monthly cost of owning the property:

- Principal and interest payments

- Property taxes

- Homeowners insurance

- HOA fees, when applicable

This is often called PITIA:

Principal + Interest + Taxes + Insurance + Association dues

A higher interest rate, larger loan amount, higher property taxes, or HOA fees can increase the monthly debt service and lower the DSCR.

Important: This Is Not a Generic NOI Calculation

You may see generic business-finance articles define DSCR as net operating income divided by total debt service. That formula can apply in commercial lending and broader business-finance analysis.

For the residential DSCR loan programs discussed here, however, lenders typically use the property’s qualifying monthly rental income and compare it to the monthly PITIA payment. Do not assume that operating expenses, capital expenditures, property-management costs, vacancy assumptions, or other expenses will be calculated the same way across every loan program.

The lender’s current guideline controls the calculation.

How Rental Income Is Used for DSCR Loans

The rental income used for a DSCR calculation depends on whether the property will be used as a long-term rental or short-term rental.

Long-Term Rental Income

For a long-term rental property, the lender may use:

- The full monthly rent shown on the current lease or rent roll, or

- The long-term market rent established in the property appraisal

When a long-term rental is being evaluated, 100% of the eligible rent may be used for the DSCR calculation, subject to the lender’s documentation and appraisal requirements.

Short-Term Rental Income

Short-term rentals require a different approach because monthly income can fluctuate based on occupancy, seasonality, and market demand.

For a short-term rental, lenders commonly use a percentage of the short-term rental income supported by the appraisal. A common approach is to use 75% of the appraised short-term rental income for the DSCR calculation.

For example:

- Appraised short-term rental income: $5,000 per month

- Qualifying income at 75%: $3,750 per month

- Monthly PITIA: $3,000

$3,750 ÷ $3,000 = 1.25 DSCR

The lender will determine which rental-income source is acceptable and how much of that income can be used.

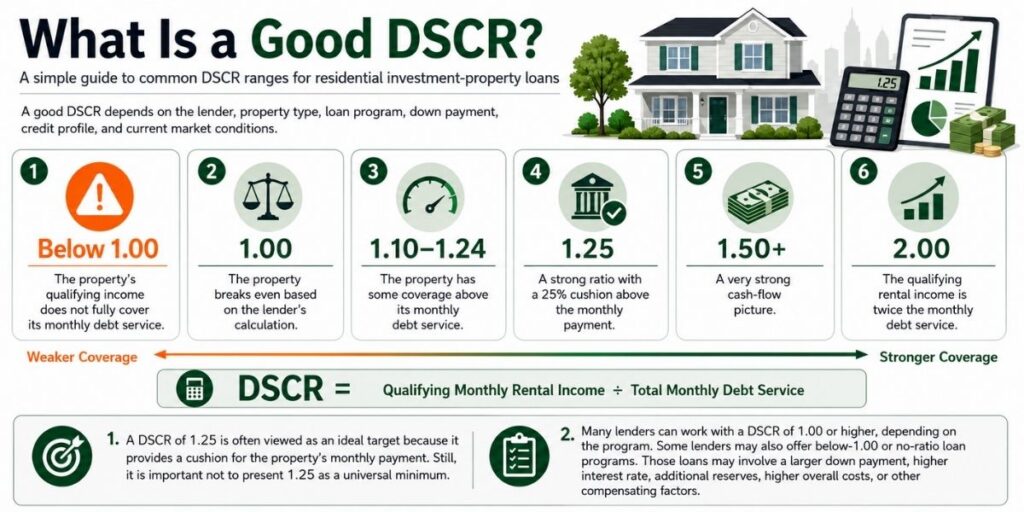

What Is a Good DSCR?

A “good” DSCR depends on the lender, property type, loan program, down payment, credit profile, and current market conditions.

Here is a simple way to understand common DSCR ranges:

| DSCR Ratio | What It Generally Means |

|---|---|

| Below 1.00 | The property’s qualifying income does not fully cover its monthly debt service. |

| 1.00 | The property breaks even based on the lender’s calculation. |

| 1.10–1.24 | The property has some coverage above its monthly debt service. |

| 1.25 | A strong ratio with a 25% cushion above the monthly payment. |

| 1.50+ | A very strong cash-flow picture. |

| 2.00 | The qualifying rental income is twice the monthly debt service. |

A DSCR of 1.25 is often viewed as an ideal target because it provides a cushion for the property’s monthly payment. Still, it is important not to present 1.25 as a universal minimum.

Many lenders can work with a DSCR of 1.00 or higher, depending on the program. Some lenders may also offer below-1.00 or no-ratio loan programs. Those loans may involve a larger down payment, higher interest rate, additional reserves, higher overall costs, or other compensating factors.

DSCR Loan Calculator: Calculate DSCR Before You Apply

A DSCR calculator can help investors estimate whether a property may qualify before making an offer or applying for financing.

To calculate DSCR, gather these monthly numbers:

- Eligible rental income

- Principal and interest payment

- Property taxes

- Homeowners insurance

- HOA fees, if applicable

Then use this formula:

Monthly Rental Income ÷ Monthly PITIA = DSCR

DSCR Calculator Example

A long-term rental property has:

- Monthly lease income: $3,200

- Principal and interest payment: $1,850

- Property taxes: $420

- Homeowners insurance: $160

- HOA fees: $120

Total monthly debt service:

$1,850 + $420 + $160 + $120 = $2,550

DSCR calculation:

$3,200 ÷ $2,550 = 1.25 DSCR

This property has a 1.25 ratio based on the rental income and monthly housing payment.

A DSCR calculator is helpful for planning, but it is not a loan approval. The final calculation will depend on the lender’s guidelines, appraisal, property taxes, insurance quote, HOA dues, loan terms, and interest rate.

DSCR Loan Requirements for Investment Properties

DSCR loans are designed for non-owner-occupied investment properties.

The borrower must certify that they will not occupy the property as a primary residence or second home. Living in the property would undermine the way the loan is underwritten, because qualification is based on the income the property is expected to generate as a rental.

Common DSCR loan considerations include:

- Investment-property occupancy only

- Credit score and credit history

- Down payment or equity position

- Cash reserves

- Property type

- Rental-income documentation

- Long-term versus short-term rental strategy

- Loan amount and loan terms

- Interest rate and overall costs

A down payment of 20% or more is common for many DSCR loan programs. Most DSCR loans also do not require traditional mortgage insurance, although lenders may have their own loan-to-value, reserve, pricing, and credit requirements.

The Mortgage Architects currently focuses on residential investment-property financing, including smaller multifamily scenarios of roughly 10 units or fewer, subject to available lender guidelines. Larger commercial financing is outside the scope of this guide.

DSCR Loan vs. Traditional Mortgage Qualification

A conventional mortgage usually focuses heavily on the borrower’s personal income, debts, credit profile, and debt-to-income ratio.

A DSCR loan takes a different approach.

Instead of asking whether the borrower’s personal income can cover the mortgage payments, the lender asks whether the property’s rental income can support the property’s monthly debt service.

That does not mean a DSCR loan has no underwriting requirements. Lenders still evaluate the overall risk of the loan. But the DSCR calculation is not the same as a traditional DTI calculation.

This can be useful for investors who:

- Are self-employed

- Have complex tax returns

- Own multiple rental properties

- Want to qualify based on property cash flow

- Prefer not to use traditional income documentation as the primary basis for qualification

- Are purchasing or refinancing a long-term or short-term rental property

What Happens When the DSCR Is Below 1.00?

A DSCR below 1.00 means the property’s qualifying rental income does not fully cover the proposed monthly debt service.

For example:

- Qualifying monthly rental income: $2,400

- Monthly PITIA: $2,700

$2,400 ÷ $2,700 = 0.89 DSCR

That property does not support the proposed monthly payment based on the lender’s DSCR calculation.

Possible ways to improve the scenario may include:

- Making a larger down payment

- Reducing the loan amount

- Choosing a different loan term

- Paying points to reduce the interest rate

- Refinancing with a different structure

- Finding a property with stronger rental income

- Exploring a below-1.00 or no-ratio DSCR program, if available

The best option depends on the investor’s overall goals, the property, and available loan programs.

How The Mortgage Architects Can Help

The Mortgage Architects helps real estate investors look at the financing side before they commit to a purchase, refinance, or portfolio expansion.

We can help you review:

- Whether the property’s expected rent may support the proposed mortgage loan

- Long-term versus short-term rental-income options

- Estimated DSCR based on monthly rent and PITIA

- How changes in down payment, interest rate, or loan amount may affect cash flow

- Whether a standard DSCR loan, below-1.00 program, no-ratio option, or another investment loan may fit the property

- Which documentation may be needed for the lender to review the file

The goal is to help you understand the numbers before you make a move.

Preguntas frecuentes

DSCR stands for Debt Service Coverage Ratio. It measures whether a property’s qualifying rental income can cover its total monthly debt service.

For a residential DSCR loan, the formula is:

DSCR = Qualifying Monthly Rental Income ÷ Monthly PITIA

PITIA includes principal, interest, property taxes, homeowners insurance, and applicable HOA fees.

No. The DSCR loans discussed here are for investment properties only. Borrowers must certify that they will not occupy the property as a primary residence or second home.

A DSCR of 1.00 means the property’s qualifying rent equals its monthly debt service. It is a break-even ratio with no additional cushion. Some lenders may approve a 1.00 ratio, while others may prefer a higher minimum DSCR.

No. A DSCR of 1.25 is a strong benchmark, but lender requirements vary. Many lenders can work with a 1.00 ratio or better, and some programs allow lower or no-ratio options with different pricing and requirements.

For long-term rentals, lenders may use the current lease or rent roll, or market rent supported by the appraisal. Eligible long-term rental income may be used at 100%, depending on lender guidelines.

For short-term rentals, lenders commonly use a percentage of the rental income supported by the appraisal. A common guideline is to use 75% of the appraised short-term rental income.

Many DSCR loan programs focus primarily on the property’s rental income instead of traditional borrower income documentation. Lenders may still review credit, reserves, assets, property details, and other underwriting factors.

Most DSCR loan programs do not use traditional mortgage insurance. However, borrowers should expect lender requirements around down payment, reserves, credit, loan-to-value, interest rate, and overall costs.

No. Debt-to-income ratio compares a borrower’s personal income to personal debt payments. DSCR compares a property’s qualifying rental income to the property’s monthly debt service.

This article is for general educational purposes only and is not a loan approval, commitment, or guarantee of financing. Loan programs, interest rates, costs, property eligibility, rental-income treatment, and minimum DSCR requirements vary by lender and may change.

Related Resources

What Credit Score Is Needed to Buy a Home in Today’s Market?

Cash Offer Loan Program: How to Compete Like a Cash Buyer Without Being Rich